Top of the Pops

Note that tomorrow I’ll do a Eurasia brief slightly different in layout than usual. Experimenting still to figure out intervals for products, how to tweak layouts or else just to improvise each time, etc.

Brent crude almost hit $46 a barrel on news of AstraZeneca’s 70% successful vaccine. The market’s clearly still grasping for any good news since vaccines are demand-positive developments. France now says that the EU is going to have 6 vaccine contracts within days, so we’re moving into the next phase of the economic crisis: everyone’s scrambling to implement vaccination programs and find ways to get things back to normal as fast as possible after riding out this year. OPEC’s betting on demand recovery to net growth led by China and India with a little help from Latin America and less from the Middle East based on its November report. The price story right now is demand, but OPEC’s numbers show US production is only down about 1-1.1 barrels per day:

It’s going to come back if vaccines lift prices faster than expected, which will then send them crashing back down. There are legitimate concerns about geology and the exhaustion of the highest performing wells in the Permian, but the underlying supply dynamic pre-COVID hasn’t yet changed. Only this time, conventional and offshore projects are going to be even leaner and smaller companies — better suited to develop projects with a short to medium-term production life and to cut costs — are going to exploit openings on the market where oil majors retrench spending, protect dividends, and pivot more heavily into natural gas and renewable energy.

What’s going on?

A shakeup for Russia’s development institutes is one of those things that’ll pass completely under the radar in Washington and probably not receive that much in the way of ink, but is an important indicator about institutional politics. The Bell labeled it a ‘cleaning', and it looks like a power grab for Igor Shuvalov at VEB.RF who, having left his government post in May 2018, wants a bigger piece of the National Goals action. 8 institutes including those at Skolkovo and Rosnano are being handed to his team, while others are similarly absorbed elsewhere or eliminated. Russia is prone to the over-bureaucratization and duplication of functions because of how weak formal institutions are compared to individuals. Reducing the number of avenues for lobbying via these institutes is probably a net good. But Shuvalov has been setting up VEB.RF targets for 2021 to show some scalps of late, Anatoly Chubais’ removal from Rosnano suggests that there’s a ‘there’ there.

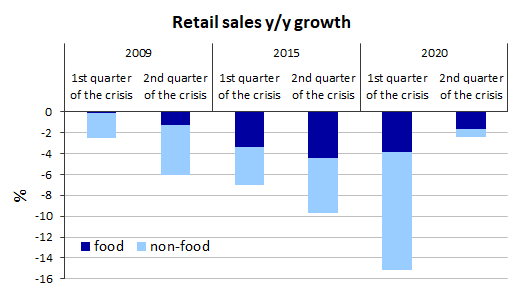

MinEkonomiki figures suggest that a decent recovery in retail is not translating into much stronger growth or better topline GDP data as of yet. From Tatiana Evdokimova (a much wieldier graphic compared to that run in Kommersant):

Retail turnover for staples and non-staple goods is only down in the range of 1.5-3%, which goes to show that Russian consumers have redirected their spending successfully towards online platforms. But much of that recovery hinges on people having a financial runway to deal with lost or lower incomes, which suggests that this may not be sustainable past the end of the current policy support in place. Crucially, however, GDP is still down 3-5%. Domestic demand at 2019 levels is too weak to return Russia growth. The current account conundrum lives on.

Agricultural exporters are requesting that PM Mishustin look at applying an export duty on grains so as to head off domestic price inflation. The article leads with a great example of how cross-sector challenges with price controls, underinvestment, and inefficiency create a drag elsewhere. Cereal grains are used to feed pigs. Pork prices have been held down by producer preference, likely pressure from the government, and trade competition, but the cost of imported veterinary medications for swine have risen 15%. Since domestic pharmaceuticals are stretched thin and inadequate to meet supply and/or quality needs, an export duty is a more effective means of lowering feed costs than quotas. Russia’s now a top-5 pork producer according to the USDA. The logic applies to other subsectors as well. MinSel’khoz is going to have to weigh different inputs against each other for 2021 since grains are in high demand globally and price inflation would soon follow.

MNCs and wholesale importers are complaining to the Federal Tax Service (FNS) that it is completely unreasonable to account for interest payments on debts incurred within the company between subsidiary and parent firms as a withdrawal of profits from taxation. In effect, the tax service now assumes that any attempt to raise working capital by borrowing from an affiliate or subsidiary firm from abroad is an attempt to avoid paying taxes on profits in Russia. Borrowing is necessary to sustain firms in the frequent gaps between production, sales, and distribution along the supply chain. But obviously there are a ways to engineer one’s tax burden as such that receipts owed are decreased, and a firm could also dodge borrowing at market rates in Russia if done right. The FNS is clearly raising additional revenues wherever it can right now, but if there isn’t a shift towards resourcing the agency to assess individual cases, international firms are going to find the Russian market less attractive.

COVID Status Report

Daily infection caseloads climbed past 25,000 yesterday, again with the regions and regional cities accounting for growth instead of Moscow and St. Petersburg. There’s no sign of any slowdown, though the growth rate across Russia regions appears slow and steady according to official data. United Russia in Nizhny Novgorod is now proposing to make calls to COVID hotlines at care centers free and to provide special rates for taxis taking people to see doctors. Policy improvisations like that matter a great deal in trying to get people in to see health providers while the healthcare system strains. Per Mediazona, Russia’s seen 106,000 excess deaths over 2019 figures for April-September, an increased death rate of 18% nationally over 2019. It’s not COVID that’s the cause directly, but rather losses of life from interrupted care as hospital beds fill up, lockdown and related measures affect people’s healthcare and health, and so on. The wider spread damage to public health and trust is visible in the banking sector given limited state support:

Title: Number of licenses for credit organizations withdrawn or annulled

Green = withdrawn Blue = annulled

It’s expected that as many as 35 banks are likely to go under next year, a bit over 9% of the total banks in the sector. Recession continues to drive consolidation and a banks expect weaker balance sheets as revenues decline with the end of policy support in sight, then likely to trigger a drop off in borrowing and weaker retail and home demand.

The Unplanned Economy

Vedomosti ran a story last night noting polling data that found that 29% of Russians want to try their hand at entrepreneurship and start their own businesses. Only 7%, however, are aiming to do so in the next 3 years. Seems most see it more as a possibility a far as 7-10 years down the road. The dynamic is a crucial one to grapple with. Efficiency gains from Russian SOEs, parastatals, and its largest privately-held firms should, in theory, increase labor productivity at the expense of employment. Larger firms are not as good at creating net job growth as newer ones for the simple reason that once you achieve certain efficiencies of scale and access to capital, cost cutting tends to be the primary means by which better returns are realized more reliably (since better margins improve performance during recessions and stagnant growth periods) and innovation is likelier to take place in a small firm trying to solve an old problem a new way. That doesn’t apply to capital-intensive R&D but the logic stands. If the Russian economy is to achieve any sort of dynamism to hike its growth rate past 3-3.5% annually — and therefore increase its share of the global economy — it’s going to require more SMEs.

60% of the respondents keen on starting businesses were under 34 years old, which goes a long way towards clarifying why the results from Opora Rossii are a good news, bad news development. As we can see from the following breakdown of those who thinks things are going in the wrong direction in Russia, younger Russians stuck in post-graduate idles trying to start families and so on are likelier to be pessimistic as those slightly older than them begin to access more social support as they age:

Entrepreneurship is just as often (if not more often) a response to scarcity and crisis as it is some innate social drive to build something of one’s own. There’s also, in some contexts, a greater deal of security in owning a business or businesses and being able to use money earned to invest into longer-term means of generating income. Rosstat figures from January show that as of 2018, SMEs accounted for a lowly 20.2% of the economy, a decline from previous years. The last oil shock strengthened consolidation and wiped out a lot of business as it turned into a bank sector crisis and it’s important to remember that a not insignificant chunk of that 20.2% will be comprised of SMEs that are contracting for the oil & gas sectors. That doesn’t diminish their relevance, but it does pose problems within the OPEC+ framework restraining output and due to lower prices. Smaller contractors without political ties or heft lose their contracts first on projects where final investment decisions are delayed and so on.

Anyone keen to start their own business, but planning on waiting more than three years, has a massive problem: they have a limited idea if the service or product they aim to provide will be in demand in quantities sufficient to sustain a profitable business. So really, the polling data showing a rise in the number of entrepreneurs-in-waiting reflects a broader crisis in the Russian economy, this time linked more with COVID, but I’d argue still evolving out of the exhaustion of Russia’s post-Soviet growth model in 2013 before oil prices crashed in the second half of 2014. Planning horizons for existing businesses are shorter in Russia than in most developed economies because of how chaotic and ad hoc the policy environment is, let alone the contingent economic factors given Russian macroeconomic policy has suppressed domestic demand (and avoided running the economy hot) to fight inflation and reduce borrowing costs. In just the spring sessions between 2014 and 2019, the Duma passed 1,909 laws — I would have to hand check how many would have directly or indirectly affect economic policies or procurements — and that doesn’t touch on executive actions, regional governments, etc. For 2013 till now in the US, that figure is 1,261, very few of which would have regulatory restrictions based on the senate and most concerning business would likely entail tax cuts. The hard numbers for laws aren’t themselves proof of how disruptive the climate is, but the state changes course constantly on policy. Corruption hinders business investment and planning, but it’s uncertainty that kills business, especially when firms with the right political connections are able to punch holes in anti-trust regimes or else consistently win what are effectively no-bid tenders for state contracts.

The fact that so many people want to start businesses but are delaying making a start past 2025 in their own estimation isn’t just directly attributable to the pandemic. It clearly imposes a massive drag on planning, but the interest rate cuts from the Central Bank are supposed to be moving economic activity planned further ahead into the present by reducing the amount of savings needed to access credit and service any loans. It speaks to how austerity policies increase long-run uncertainty for economic actors at the microeconomic level while otherwise being used to improve certainty at the macroeconomic level. By Rosstat’s own estimation last year, 12.7% of Russian GDP falls into he shadow economy without being taxed or properly recorded. Would-be entrepreneurs are responding to the reality that a huge portion of the national economy isn’t even being regulated or taxed properly, the state isn’t spending enough to create demand, and personal finances are now beginning to strain despite the appearance of good news. Take the CBR’s latest on M2 money supply:

A rise in transferable deposits for households is a polite way of saying they’re saving more cause of job insecurity and wage cuts or real income declines. Other deposits are up because people are taking out more credit to get by or buy homes at lower prices now. Other deposits are in negative territory because people are drawing down illiquid assets to pay off debts or are putting more money into transferable deposits expecting expenses. Russia’s economy faces a large planning problem now that households are beginning to enter the toughest stretch of the pandemic without more support. That poll was a leading indicator of just how bad Russians actually think things are going to get. An improvement in the expected planning horizon for entrepreneurs is a decent leading indicator that things are actually looking up. I’m not holding my breath, though.

Coins of the Realm

The FT ran a piece with VTimes on Friday highlighting the possibility that the US dollar could devalue against many foreign currencies by as much as 20% next year per some investment banks because vaccines and economic recovery are weakening its draw as a safe asset. That’s an out-there forecast to be sure. Things have calmed down since since spring and the dollar now looks to be about 7% down off its March surge per its trade-weighted index. People are getting ready for a dollar-bear mindset, including the latest report that the Euro had surpassed the dollar for share for transactions via SWIFT, a slightly misleading headline since SWIFT includes in-country transactions and the US still edges out the Euro by about 4% for cross-border transactions. That number doesn’t seem likely to stick, though. The combination of vaccine news and US congress’ dithering — I truly cannot fathom anyone who respects the leadership in either party at this point — is triggering a massive outflow from the US into global equity in search of better yield now that it’s safe to stick their heads above the parapet:

If a USD devaluation of 20% were to take place, ironically, it’d be evidence of the market’s confidence that the Federal Reserve is doing everything it takes to reflate the US economy and, by extension, support emerging market exporters. As noted by Robin Brooks, the market’s still unimpressed with the European Central Bank, especially now that the recovery fund talks within the EU have stalled again:

10-year swaps show that there’s no faith in a European recovery. That’s a structural problem, not one having as much to do with COVID as European institutions are messaging. The Euro’s appreciation is a structural drag given how much Europe relies on exports elsewhere to sustain its growth prospects. I’m a bit more interested in how currency movements and commodity markets intersect going forward.

China has launched a copper futures contract denominated in yuan. While subscriptions are still low, the market’s going to express interest, especially if the CNY strengthens further against the dollar and becomes a useful hedge while Euro strength becomes Euro weakness. The relative decline of USD dominance for commodity contracts is not the death-knell for USD hegemony, but does reflect how different the geography of demand now looks. Russia’s play for the Euro (or better, Rosneft’s) was shortsighted given that China now refines more oil products than Europe does and is on pace to overtake the US for refining capacity in the near future. India is still planning to double its refining capacity in 5 years. These changes are all leaving Russia behind as it tries to politicize the use of currencies explicitly no matter the prevailing winds from the market. The real question is what happens internationally if the world’s second currency — the Euro — starts losing ground because of economic dysfunction and failure to recover post-COVID. There’s no one really quite close to the Euro out of the pack, and the relative diffusion of market share to currencies among more pretenders to the dollar throne, I would argue, increases the relative power of the USD within the obvious limits imposed depending on how usage evolves. It’s easy to look at things as they stand today as evidence of how they’ll look tomorrow. We’re only just now reaching the point at which the structural failings of Europe are showing while the Asia-Pacific, well-positioned to increase export surpluses, steams ahead with the virus relatively under control.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).