Top of the Pops

Yesterday, Russia imposed a flight ban running from April 15 to June 1 for any flights headed to Turkey. The ban followed a visit to Istanbul by Ukrainian president Volodymyr Zelensky where Erdogan restated that Turkey would never recognize the annexation of Crimea and supported Ukraine’s full membership in NATO. The ban is transparently an economic punishment presented as a health concern: Russian tourists have apparently been more worried recently about COVID-19 in Turkey lately, but not cause of the virus. That would make little sense given domestic attitudes. Rather they didn’t want to be trapped by a border closure. The loss of tourism revenues at a time when travel volumes from the West are far down adds to considerable existing stress on the country’s macroeconomic stability, particularly with the rise on US Treasury yields and stimulus plans imposing costs on emerging markets:

Service exports keep the country’s current account in balance, a great deal of that coming from resorts and related hospitality services. The lingering problem on the back burner for Moscow is that Turkey and Ukraine are, per the rosier statements from their own ambassadors and boosters, hopeful they’ll sign a free trade agreement this year that would help double trade turnover to $10 billion. That can’t touch the scale of what Russia offers Turkey and there’s much left to settle — the Turkish steel industry, for one, is panicked about a potential flood of Ukrainian imports — but economic linkages matter and can prove useful in time. Erdogan’s trapped relying on foreign policy decisions to manage domestic shortcomings. Ankara’s pursuit of closer military ties with Baku — Turkish and Azerbaijani forces conducted joint military exercises several days ago — is as much about that as it is a shot at Russia. Watch to see if Moscow cranks up the temperature in the following weeks.

What’s going on?

The government’s officially denouncing its double taxation treaty with the Netherlands, a consequence of Putin’s March 2020 order to impose a 15% tax rate on all revenues from interest or dividends. The current agreement with Dutch authorities allows foreign firms to withdraw revenues from Russia at an effective tax rate of 2-3%. Putin’s executive order set out that all double taxation treaties would have to be revised, and if they couldn’t be, unilaterally ended. Last August, MinFin proposed the Dutch raise their rate for revenues withdrawn from the country from 5% to 15%. This went over like a lead balloon. Without a deal, the current treaty will expire on January 1, 2022 and Russia will raise rates for interest revenues on Dutch entities to 20% if there isn’t an agreement. Dividends for Dutch entities operating in Russia and passing money back will rise to a 15% rate and if MinFin adds the Netherlands to its black list, then dividends passing through Dutch subsidiaries declared by Russian firms i.e. declared there and not in Russia will be raised to 13%. In effect, the Russian government is negotiating through bullying while also making Russia that much less attractive for foreign multinationals to have to deal with in case they decide to revise rules in the future in a similar ad hoc manner. A large number of Russian holding companies would have to be restructured as a result, an annoyance but not a huge hindrance so long as they don’t mind the legal fees. Oddly enough, the Biden administration’s push for a global corporate tax minimum aimed at offshore tax havens like the Netherlands might make it easier to renegotiate in the future. The scramble to increase fiscal capacity without taxing people and call it good governance continues.

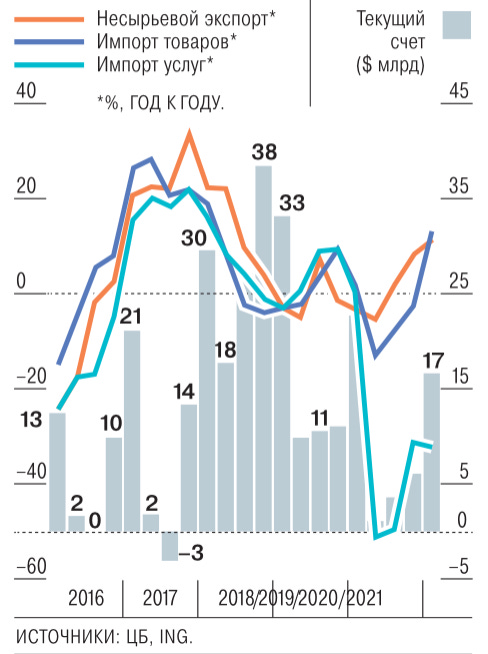

The trade data for 1Q surprised observers — Russia’s current account surplus came in lower than expected at just $16.8 billion. The recovery in oil prices and rising non-oil & gas commodity export prices haven’t helped much:

Orange = non-resource exports Blue = goods imports Cyan = services imports

Columns = current account (US$ blns)

The increase in non-resource exports matches closely a recovery in goods imports that appeared to be overshooting them in size from the last of the data. For comparison, fuel export earnings for 1Q reached $45 billion, the lowest figure since 3Q 2017 when oil was $8 a barrel cheaper. OPEC+ cuts really are weighing on the current account. There’s also been a correlated rise in Russian firms’ and investors demand for foreign assets, so capital’s leaving the country while demand for imported goods continues. My current theory on the rise of imports is that firms with foreign currency earnings are scrambling to grab what they need, some of that is debt-financed consumption, but more broadly, the constant idling of the economy below its real capacity on top of efficiency-killing economic policies and underinvestment renders it more sensitive to sudden increases in demand from re-openings and mass changes in consumer behavior. I’d bet a fair bit of the import increase would also reflect e-commerce imports that first head to distribution sites before going on to consumers hunting for bargains. Could be other causes as well, but have to factor in that the ruble’s weaker of late.

A bunch of large Russian wheat exporters have suspended purchases from Russian producers because the loss of earnings incurred by the price control export duty increase is too much to bear. As of now, the gamble is that purchases for export abroad resume once the duty falls after June 2 or else when the excess supply on the domestic market dovetails with the new harvest crashes prices downwards. Kommersant’s reporting that Louis Dreyfus, Bunge, KZP, and Sierentz Global Merchants have all effectively left the Russian market for now, with Bunge’s departure likely also linked to the sale of a grain terminal in Rostov to Russian firm “Agro-Land Trade”. The current duty costs $59 a ton. Russia milling and feed wheat cost in the range of $225-245 per ton right now. The duty is insane and no one wants to pay it since it’ll fall to $21 a ton if wheat’s at $230 fo exporters after the June 2 shift. The end result of this nonsense is that producers won’t be able to sell volumes, or else will have to keep marking down prices, denying them profits they need for capital plant going into the next growing season and, depending on their contracts with domestic vs. international wholesalers, potentially some foreign currency earnings as well. But this raises market risks of squeezes on supply abroad if other producers can’t match the output gap left by a loss of Russian exports, effectively “exporting” inflationary pressure via a policy approach that may well induce more of it domestically in the future through underinvestment or less efficient investment in production. Russian exporters and MinSel’khoz are confident Russia will maintain its position as the world’s leading exporter. I’m inclined to agree. They just didn’t have to go this route to do so.

Citing sanctions risks and political risks from rising Russian-Ukrainian tensions, JP Morgan announced that it had reduced its portfolio of Russian assets, namely selling off OFZs it held as well as some rubles. Manfred Weber, leader of the European People’s Party in the European Parliament and a supporter of potentially cutting off Russian access to SWIFT, said the move was justified. The fear now is that JP Morgan’s announcement will trigger a move out of Russian assets among more and more institutional investors. The ensuing capital flight and asset rotation would likely weaken the ruble to 80 or higher against the USD and 95 against the Euro. But JP Morgan is also shifting money out of developing markets more broadly at the moment because of the rise in US Treasury yields, expectations of higher inflation in the US, and most importantly, strong US growth. It seems quite unlikely to affect macro indicators in Russia overall, with any weakening of the ruble a reflection of the rising political risk attached to it because of how Russia has approached the recent escalation of troop deployments without offering any counter-balancing diplomatic assurance since the intention is to coerce. The risk premium on the ruble has shot up since Biden’s “Putin’s a killer” comment and tensions with Ukraine worsened. But the story goes to show that you can’t blame sanctions risks for everything — markets are also pulling back from EMs and Russia’s a pretty poor one to be invested at the moment — and not even Biden’s explicit statement that he does not intend to order any sanctions on sovereign debt calmed the market. Either no one believes him, which I highly doubt, or more likely, no one has trust in the Russian economy’s prospects, there are better, safer options elsewhere, and the ongoing course of Russian policy has given institutional investors an easy way out as things get worse.

COVID Status Report

8,173 new cases and 338 deaths reported. Tracing the decline shows a continued fall, if very slow, in the regions with a slight uptick or stagnation in Moscow. What that suggests to me is that Moscow is likelier the tell for the national story than the regional data. The decline rate for the last week was a paltry 0.9% and it mirrors the pattern shown by the 2nd wave in concerning fashion:

The vaccines may be helping some, but this looks eerily like the progression of the week-on-week data from late August into September. Rospotrebnadzor has admitted that the number of cases of the Kent strain from the UK was up to 128 — note that while it isn’t deadlier, it has been found to affect young people more heavily — and given the persistent gaps in capacity, it’s probably safe to assume that figure is a bit higher in actuality (though not yet cause for alarm). Worse, the state appears to be remarkably spendthrift in its approach to the vaccination campaign, at least if we take the federal budget as an indicator. For the 2021-2023 budget cycle, a mere 76 billion rubles ($984.2 million) is to be spent on vaccinations. It sounds like a lot more than it is given the capacity of the state to spend more and the need to do so, especially with the public’s reticence over vaccines in general.

Rent Out of Shape

Carbon border adjustment mechanisms get most of the press when looking at the potential impact of EU green policies on Russia, but there are ways by which the bloc can effectively “export” carbon pricing without an adjustment mechanism onto external markets in a manner that will force them to adjust quickly. In this case, I’m thinking of shipping. A coalition of shipowners — Greek and Swedish apparently — and the European Federation for Transport & Environment are lobbying the European Commission to create a carbon pricing system for maritime trade and shipowners that incorporates travel and emissions that occur external to the bloc so that it doesn’t discriminate against short-haul shippers only operating between EU member state markets. By including voyages between the EU and third countries, European shipowners would theoretically be at a disadvantage if there wasn’t a levy on other ships calling into European ports. The likelier idea, in this case, would be to make use of the Automatic Identification System (AIS) legally required internationally for all ships with a tonnage of at least 300 tons or else all passenger ships since it tracks all trips. European companies would likely then be required to monitor and report fuel used, cargo carried, distance traveled, and similar relevant information from internal EU policy deliberations going back to 2014. If external firms fail to meet requirements, it’s conceivable that a system of levies or similar mechanisms privileging access to firms who match EU criteria could be used. It’s also crucial to acknowledge that pricing isn’t ever enough, it has to be supported by increasingly aggressive regulatory requirements to lock in greener technology, capital goods, and more.

Maritime carbon pricing is an area where explicitly transnational markets can create a pressure point less readily apparent than internal and external carbon adjustments to competitively advantage domestic manufacturers against cheaper, dirtier competition that fails to decarbonize. It shoves the costs primarily onto firms themselves, firms that in the case of international shippers, generally have access to analogous equipment regardless of national registry or a home market and are only forced to factor in the additional carbon overhead for Europe in this case. That may make things more expensive for Europeans to import on a comparative basis initially — theoretically positive for re-shoring efforts — but it also creates a larger international lobby to adopt similar systems elsewhere if they have to absorb higher costs by buying greener to maintain their earnings. Changes in end cost can end up losing shippers’ market share and profits as well as further incentivizing investments into cleaner and more efficient engines, fuels, and designs above and beyond the impact that IMO 2020 has had reducing demand for the dirtiest fuel oils used in the industry. All of this requires large markets to not think in terms of optimal prices, but the optimal balance of prices weighed against externalities and related opportunity costs from a failure to incorporate those externalities into pricing. If the proposal on maritime carbon pricing picks up steam in Europe, the logical question is what happens next if it’s adopted and what are potential corollary implications for domestic policy in Russia?

Take Moscow’s initiative to expand use of the Northern Sea Route, thereby justifying the often wasteful use of federal resources in the Arctic. If ships transiting the route to European ports have to add in carbon costs and other externality pricing, it can alter the economic attraction of using the Arctic route. Thankfully, Russia has nuclear-powered icebreakers, but one can imagine it’s not that difficult to establish a baseline level of additional emissions from the use of a pilot boat in a canal or other waterway and add up a cost there. If Russian authorities fail to harmonize practices with EU requirements and, crucially, the Suez Canal, the NSR loses some of its appeal. The time gain for travel also matters less on pricing grounds the cleaner the fuel used to power a ship is since it contributes less to the overhead. Shippers might be competing to use dirtier ships on faster routes and vice versa initially, but this would all fall apart if the US ended up aligning itself with EU policy as China — then trapped by the combined weight of its two main trade partner markets — would most certainly have to follow suit. This then affects one of the most important import substitution targets for Russian SOEs since 2014: shipbuilding.

I tried to dig up data on shipping quickly, but it takes a bit more time. Instead, I’ve pulled a snapshot of the % share machinery and related equipment takes up for fixed assets at the sector level as well as the % share of investment activity going into reconstruction and modernization:

As we can see, the amount of money invested into modernizing existing plant has fallen since stagnation started in 2013 without any real interruption while the % share of fixed asset investment taken up by machines and other productivity enhancing equipment has been basically flat for agriculture, resource extraction, and value-added production. The first two are pivotal exporting sectors that should be the focus of productivity gains to be able to redistribute rents elsewhere as needed and the latter, while not necessarily bad, is problematic if the net level of investment modernizing existing productive capacity is falling. Rosneft has been a key offender, ploughing billions of dollars into the Zvezda shipyard complex, including unnecessarily building up its own capacity to supply materials, while ensuring that state policies mandate other SOEs and parastatals “buy Russian” from them. But if maritime regulations begin to affect the economic competitiveness of anything Rosneft makes on the basis of future carbon costs that buyers have to factor into operations, they have to adapt. That could take the shape of only using Russian ships for cabotage purposes, trading on its own territory and avoiding costs elsewhere. That could equally entail an increase in the level of subsidies to Rosneft as well as buyers if Russian policy doesn’t keep pace. The less is spent each year modernizing production, the more grievous the harm from carbon pricing will be for exporting industries, the NSR, and rentier moneypits like Zvezda and the shipping industry in general.

Zooming out to a high-level view, it becomes clearer that the entire logic of “sovereign” globalization adopted by the de facto economic consensus for over a decade now only made sense in a world where externalities weren’t a matter of political and commercial dispute and contestation. There aren’t any means to subsidize away or hide the end goal of decarbonization. It has to take place, and without access to imports from those much better at doing it, costs in Russia will rise considerably as that process unfolds. Mishustin’s been tasked with gathering the government together to work out a large economic program for Putin’s April 22 address meant to foster an explosion of investment activity across the economy. It’s a huge moment for the regime, not because of the elections ahead, but because of the necessary shift in economic logic to manage carbon adjustments in different sectors as international political pressure grows. The Soviet economy collapsed, in fair part, as a result of massive over-investment that created a set of political lobbies invested in maintaining the growth model at all costs. By the 70s and 80s, that meant increasing debt levels and oil export earnings were needed to avoid painful economic adjustment as the high growth delivered by the industrial investment-led model evaporated. Consumers needed to be able to consume more and inefficiency began to eat it alive. The model under Putin has been the reverse, a political economy built on accumulation and under-investment for the sake of ‘stability’ eventually creating the same types of political trade offs, even if the political stakes are far lower for now.

Global investment into the energy transition has grown massively, but even these levels are pathetically inadequate if we’re going to meet the intended targets to ward off much larger temperature increases. National spending levels are going to keep rising, though:

The energy transition entails a massive jump in gross investment levels just about everywhere as well as a % increase in the share of investments into modernization in the early going until the market has adjusted fully and all new plant is already built to green spec. Maritime carbon pricing is a small example of the problem, but reveals just how large the economic shock to the regime is bound to be as we get closer to implementing these types of policies. What’s more, the attempts to insulate the budget and macroeconomic stability from oil prices have heightened the ruble’s exposure to political risks since the currency doesn’t benefit from higher prices that much. If in 2014, you had told the Kremlin the ruble would stop falling in value because the president of Ukraine, a former comedian, assured markets by saying he was prepared for diplomatic talks with Russia, they’d have scarcely believed you. But the reality of “Fortress Russia” is that every move to insulate itself has come at the expense of the investments it needs and increased its macroeconomic exposure to policy decisions, rhetoric, and mood swings in Washington, other foreign capitals, and on financial markets. Moscow’s learning about opportunity costs the hard way.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).