Top of the Pops

The World Bank’s latest report on the state of Russia’s integration into global value chains was a good skim combining all of the things we basically know, with some added details that speak volumes to the structural problems facing trade. The following is a simple comparison of weighted average tariffs on primary products vs. manufactured products:

Russia protects its own extractive industries with higher tariffs on resource imports, but leaves considerable room to further drop tariffs on manufactured product imports — arguably necessary at this stage to try and build up intermediate stages of value chains. What really struck me more was the high cost of Russia’s terrible compliance regime for trade. According to World Bank estimates, the documentary and border compliance procedures take a combined 91 hours on average vs. 14 hours in Turkey and 4 hours in the US. As a result, a single TEU of goods costs $670 vs. costs of $230-350 in China, India (the world’s second worst performer for these metrics), and the US. The complicated system of regulatory rents the customs service (and FSB officials who’ve moved in on its turf) have deeply embedded amount to a significant tax on exporting industries, leading to higher failure rates for SMEs and narrowing the scope of businesses that can compete. It’s easy to blame the network effects other industrial exporters benefit from once they establish an advantage, but it’s pretty obvious Russia’s got itself to blame on this one. Sectoral subsidies are then inefficiently allocated because they’re masking lost revenues/profits from contracts lost and higher export costs that have to be financed by Russian banks and financial institutions with a frequently higher cost of borrowing and greater currency risks. Reforming customs processes would provide a much greater long-run stimulus than most spending plans would.

What’s going on?

Two policy stimuli seem to doing the heavy lifting for national industrial production data — mortgage subsidies are raising demand for housing (for now) and panic over COVID and poor public health efforts has bumped up pharmaceutical output on top of the surge in vaccine production. Demand isn’t just consumers worried about getting sick. It’s nearly doubled for diagnostic medications used by medical care providers (production rose 5.3% just between Oct. and Nov. while vaccine production in that timeframe rose by 54% and production of flu vaccines contributed as well). Price controls are likely dampening the potential production response for non-vaccine medications, but the sector has benefited perversely from the patchwork nature of the public health response. The relative weighting between sectors’ share of industrial output is something I have to dig more into, but I suspect that COVID has altered it slightly.

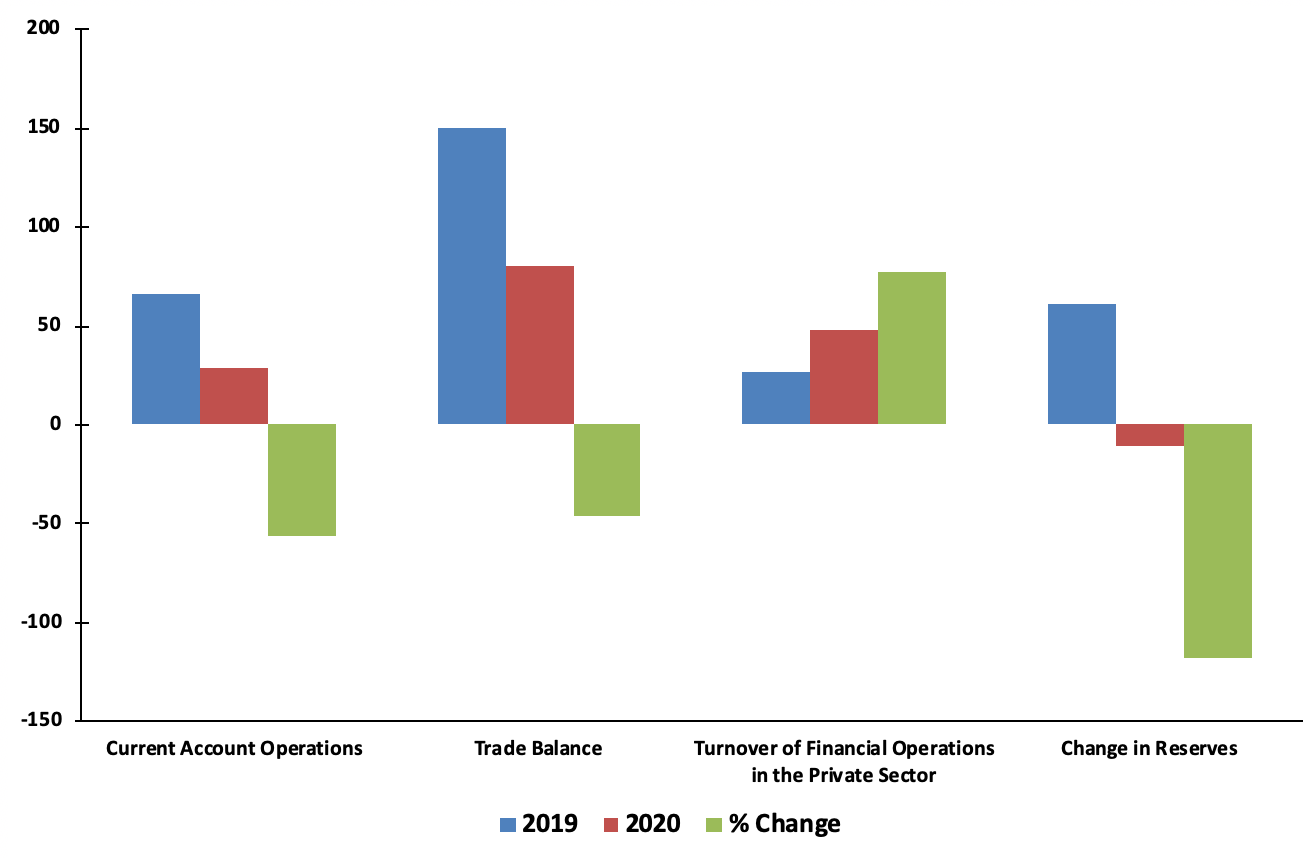

The World Bank is now forecasting that Russian GDP in 2020 will only contract by 4%, better than the 5% expected from earlier forecasts, but warns that the country’s lack of integration into global value chains poses a structural drag on healthy long-run growth. The Bank’s report on the recovery — linked here —shows the main driver of Russia’s smaller-than-expected contraction was commodity prices:

More interestingly, existing social policies seem to be blunting the impact of poverty increases due to unemployment, but that unemployment rose across all regions between 2Q and 3Q. It’s hard to imagine that the safety net is going to function adequately if there isn't stronger jobs recovery, particularly with state policy now moving to head off inflation for consumer staples. For now, the gamble is still that a commodity market boom will return Russia to growth. But the next boom will likely further concentrate investment and revenues in the extractives sector, but outside of oil & gas, to the detriment of the development of trade in finished or intermediate goods and services.

Moscow’s government-backed home insurance program is coming to an end after 25 years, forcing residents to find more expensive plans from private insurers without the participation of the city government from now on. The program was initially meant to help sustain the development of a private market, which now effectively exists. Numbers weren’t reported, but the AKRA estimate places annual premium collection via the existing program at 4 billion rubles ($54.96 million). The program was the model for a federal copycat that has been passed into law but isn’t operating. On one hand, it raises costs for consumers, which inevitably hurts more in Moscow. On the other, insurance companies provide an important pool of financial resources to be invested. Overall, I’d argue it’s a net positive to rollback what are effectively subsidies in general, but doing so mid-crisis seems foolish since the pandemic’s economic fallout will lead to a net decline in insurance policies agreed as people pinch kopeks.

Fears that Artyomev’s departure from the Federal Anti-Monopoly Service would weaken its ability to influence key regulatory decisions seem to be coming true. FAS has reportedly opted to compromise its position on the relative strength of the existing law “on the protection of competition,” particularly as concerns intellectual property and economic activity in the tech sector. The ministries and IT companies were harsh critics of FAS’ previously tough line on antitrust immunity as it sought to expand its power to regulate markets prone to oligopoly and monopoly formation (think tech), not just the natural monopolies such as RZhD and pipeline operators it was created to manage. FAS has rewritten its 5th antimonopoly package — a legal revision to its charter — to only extend oversight to internet platforms, medications, patents, and know-how, excluding other aspects of intellectual property and intangible assets as well as anything under franchising agreements. Though FAS has always acted selectively, it realistically sought to do so in the past to maintain and encourage FDI. It now looks like the institution, still relevant for regulatory disputes, is about to see some (relative) rollback of its powers after 5 years expanding its remit to include the regulation of ports and ecological concerns from business.

COVID Status Report

Cases rose back above 28,200 thanks to increases in Moscow — 587 deaths were recorded yesterday. If you look at Moscow’s peaks and troughs since November, there’s a net downward trend (slow it may be) while cases in the regions still seem to be flattening:

Black = Moscow Red = Russia Blue = Russia w/o Moscow

The conversation is shifting now to why it is that Russia’s excess death rate during COVID came in at a 15.9% year-on-year increase over 2019, twice as bad as the US and 7 times as bad an increase as in Germany. One United Russia rep at the party’s online social forum proposed that all frontline workers not in health specifically, but teaching children, caring for sick people, etc. be insured by a government program of some sort. A programmatic stump for Russia’s own healthcare revolution isn’t in the offing, but the rollout of the vaccine is setting up a series of uncomfortable questions for local and national authorities as to why it is that the broader healthcare system was often overwhelmed. Surely the lack of public faith in institutions tasked with ensuring its safety and health is part of the story. 22% of Russians are reportedly planning to travel for New Year’s. That’s not going to help come January. But it cuts as well to the impact of austerity budgets over the last 6 years.

Oiling Frogs

No, frogs don’t wait to be boiled alive when the temperature slowly ramps up, but the image is certainly a captivating one when describing the costs of inaction in the face of gradual change. The kettle’s been set to boiling for the oil market since 2014-2015, however. The current rally is therefore a test of whether that water’s no longer being heated up. For the first time since the beginning of March, Brent has climbed past $50 a barrel. The experts quoted by Vedomosti place Brent in the $47-49 a barrel range by the time Biden is inaugurated thanks to the lack of substantive good economic news. John Kemp from Reuters mirrors the sentiment with the current rise more indicative of the futures market lifting on vaccine optimism rather than physical market tightening as much as is reflected by price:

Goldman Sachs is now selling the line that oil’s set to rebound to $65 a barrel next year. The 2021 outlook comes down to how much non-OPEC+ production has been taken off the market, how much is reduced investment in US shale output here to stay or waiting for a price rebound, and will underlying demand be enough given existing slack capacity. The picture is decidedly mixed, and Russia is unlikely to be planning any major investment push outside the parameters of OPEC+, especially since the current oil price goes a long way towards balancing the budget faster. If oil hangs north of $45 a barrel for at least the next month, that’ll help stanch some of this year’s bleeding when you take a quick look at the macro balance of payments data (this is comparing Jan.-Nov. for both years):

The scale of change worked better as a column rather than a line on the opposite axis, and the financial values are all in US$ blns. As the current account surplus declines, there’s an increase in capital outflows from the private sector, largely paying off foreign-denominated debts or other liabilities in this case. The rise of non-oil & gas revenues, however, reduces the budget pressure related to the fiscal breakeven. But the market picture sustaining this change doesn’t suggest that banking on a higher oil price is a good idea for the Russian economy.

US Energy Secretary Dan Brouillette believes that oil prices will stabilize in the $55-60 a barrel range if economies open up without too much trouble, using his position to warn of the downside risks Biden poses for shale while neglecting to mention that any bans on fracking on public lands will have a minimal impact on the relevant shale plays driving US production and that larger industry players have come out against Trump’s regulatory rollbacks in many instances because they recognize that while small, independent drillers benefit, a stricter emissions regime will be essential to maintain the competitiveness of US production against that managed by European companies, especially as carbon border adjustment for trade of all stripes comes into view for policy discussions. Shale output is forecast to decline another 133,000 barrels per day in January, down to 7.44 million bpd, but the total US rig count is up to around 338 — a big rise from its nadir — and here’s the kicker: offshore oil breakevens are now generally lower than they are for US shale after shaving costs down 30% between 2014 and 2018 alone. Rystad has its problems, but it now models deepwater offshore breakevens at an average of $43 a barrel. The exact number matters far less than the general direction of travel and viability of projects for oil majors like Exxon.

The basic problem facing OPEC+ from the start was that the initial move to flood the market in 2015 may have pushed US shale firms to go bust, but it triggered a wave of cost-cutting innovation among companies that have proven they’re much better at it than their NOC peers. There aren’t many low-hanging fruit for efficiency gains in the deployment of capital without further technical breakthroughs, but it’s easy to forget that there can be periods of cost deflation for extraction that end up undermining higher-price scenarios even if shale never fully recovers or demand returns to substantive growth. There’s also the problem of crude quality. OPEC cuts to heavier, more sour oil production and Mexico’s mismanagement of oil projects has given Canada’s oil sands — a source for heavy, dirty crude — a new lease on life in the form of interest from Wall Street now that more takeaway capacity is under construction. This image of an oil market precariously balanced between demand, OPEC + Russia, and US shale was always misguided because it ignored lessons taken from the oil market regime’s shift after OPEC surrendered to market pricing power in 1986-1987. Production on the margins is all it takes to trigger significant imbalances, cutbacks of existing output or changes in the crude slate would alter the premiums and discounts on different crude blends thus changing investment rationale into existing and prospective projects, and cost deflation and innovation can outrun OPEC+’s short-run ability to balance the market. And that’s before looking at OPEC’s internal problems.

The UAE announced a discovery of an additional 2 billion barrels’ worth of crude reserves as part of its plan to pressure Saudi Arabia for more power within OPEC. Adnoc had set a 4 million bpd production target it’s reached with plans to raise output to 5 million bpd by 2030 while Saudi Aramco has discussed increasing its maximum capacity from 12 million bpd to 13 million. The demand side remains highly uncertain and short-termist. Announcements of inventory draws in the US and high utilization rates for refineries in India helped boost prices the last few days, but it turns out that it’s now stimulus talks in the US raising hopes. The strength of the US dollar is generally a proxy for what to expect next now on commodities markets, for equities, and for the reflation of economies across the globe, and it’s now weakening against major competitors. The Euro’s at 1.22 US$, which is actually a big deflationary red flag given the Eurozone’s dependence on German export competitiveness, but no one cares about European growth anymore since its a stagnant market for oil regardless. What’s better news is that the dollar has weakened some against emerging market currencies, one of the problematic mismatches from earlier in the year i.e. dollar weakening against the CNY, Euro, and Pound but not the developing economies elsewhere. Even with that glimmer of hope, there remains as yet nothing like the G-20 coordination from 2008-2009 that enabled a global recovery, even though in that case Germany and the EU were free riders exploiting the US and China with their respective stimulus plans using austerity measures and wage suppression to support Germany’s exporters.

What’s interesting to note is just how absent Russian agencies and ministries are in the process of communicating a clear outlook. Everyone’s still waiting, while the ground shifts. The oil price and demand outlook still matter most for a wide variety of Russia’s macroeconomic indicators, yet oil & gas are starting to lose their grip on Russian equities and financial markets. Tech now accounts for about 8% of MOEX and oil & gas may have to settle for a steadily declining share of the volume of money on the market. Look at MOEX’s sectoral indices. Lhs is US$ blns for total volume, % share from the lines:

Sber is going to keep rising in the future, even if Rosneft will be nipping at its heels for now having overtaken Gazprom once more to become Russia’s second-largest company by market cap. Banking & finance briefly overtook oil & gas at the worst of it, and arguably have far more scope to grow since Sber and other service providers will be tapping into the potential of various online platforms, e-payments, etc. Though efforts are now finally underway to model the macroeconomic implications of peak oil demand for Russia, what’s less clear is how the oil price cycle and outlook will feed into financial markets and investor expectations to try and make money. Mining & metals have a clear shot to challenge oil & gas for the leadership position as well depending on just how strong the incoming commodities rally ends up being (crucial to note that green policies in Europe would call for a short-run demand increase even amid economic stagnation).

The oil demand question is almost irrelevant to the price outlook past a very short window for increases because futures markets will relatively quickly realize just how fragile the supply balance was even with OPEC+ cuts in place, short-term investments for shale will return even if at a reduced clip, and offshore projects will be greenlit. But the overall picture still looks negative for any real growth post-crisis. As the financial weighting of Russian firms shifts, so will the lobbying pressure with foreign investors, especially since FDI is concentrated in extractive industries. When oil & gas start to fade, that’s when it gets interesting. Who controls which administrative resources, can arrest whom, can seize what will matter a great deal more. Hopefully Gref, tech whizzes, and bankers are up to the challenge.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).