Top of the Pops

Apologies if you’re a paid subscriber, this accidentally didn’t send to everyone!

The cold snap in Texas has become a world oil market event. Over 4 million barrels of daily output in Texas is currently offline, akin to if a bit more than all of China or Iraq’s production just vanished off the market all at once. The problem is that a full restart for wells in Texas that are frozen solid could take weeks in some cases. Even if that happens — it seems likelier shale will come back fast with the thaw this weekend — that actually isn’t that big a deal but is a huge source of pressure on OPEC+ cuts. The trouble now for Saudi Arabia is that Russia’s now happy to claim the market’s balanced, and it’s not just deputy minister Aleksandr Novak doing the comms work to suggest that. Russia’s leading oil firms met with Novak to plead for tax cuts after a series of tax breaks and exemptions worth billions of dollars were rolled back last year as part of the fiscal consolidation push. They also want to move fully onto a profit-based tax regime instead of the current phase out of export duties to be replaced (and then some) by higher mineral extraction taxes (MET). MinFin’s taken a hard line that oil firms aren’t effectively using tax breaks and doesn’t want to switch up the tax regime before 2024, stranding the oil sector with a high tax burden and a tax system where the state effectively takes most of the additional profits from higher oil prices once they climb past $35 a barrel. Companies want to up output, and higher investment into production would create more economic growth this year (at the expense of some macroeconomic stability depending on where prices fall).

As of now, Saudi Arabia plans to end its additional cuts instituted in January come April. That timeline may have to be accelerated if Texas' output is down several million barrels a day for weeks longer. Brent ICE Futures keep climbing, and soon will rest comfortably north of $65 a barrel — Lhs = $/bbl:

This is an incredibly dangerous development for oil market stability in 2020. If OPEC+ rollback cuts too fast, they swamp the market with a still uncertain recovery and while that kicks shale drillers when they’re down, they’ll still be around as the market rebalances more strongly in the second half of the year. If they don’t and prices overshoot too high, Russia risks domestic inflation risks worsening linked to a potential surge of industrial (and some consumer) imports and higher fuel costs while shale drillers will just dig themselves out and start pumping away as fast as they can since their earnings horizon for any given producing well is basically 6 weeks rather than a years to decades long arc like in Russia. Both are net bad for oil exporters. As prices rise, MinFin’s also got more leverage i.e. the relative tax burden for Russian oil producers rises in many cases and they can demand a certain level of investment in exchange for a tax break, while setting conditions on those breaks. Since output is more price insensitive in Russia above $35 a barrel, the oil sector’s bound to lose more clout during the current rally as demand growth begins to crumple under the weight of fuel substitution efforts. Ford just joined the chorus of big firms with 100% EV production targets (2030 for Europe in this case). Change is coming slower than we hope, faster than many expect.

What’s going on?

According to Ekspert RA, 33 banks — 9% of the market — face default risks in the year ahead as a result of low reserves and the instability of deposits. The Central Bank pulled the licenses of 9 credit organizations in 4Q last year (17 in total for the year) as it sought to prevent any contagion from financial fragility and defaults. Oversight efforts were somewhat curtailed by the pandemic as the focus was on maintaining sector liquidity, but now that recovery is slowly starting, more banks struggling to maintain their profitability are going to have to go. Fewer organizations were liquidated or lost their licenses in 2020 than in 2019, which speaks to the success of plugging gaps in the system using Central Bank reserves as well as the drawdown of SOE foreign currency holdings in September-October. But 51.6% of the country’s banks had a low credit rating, which is why 16 organizations voluntarily folded last year. A lower key rate reduces the spread on loans, thus squeezing bank profits some, but the bigger worry has to be the solvency of households and SMEs — large firms appear to have gotten through fine, especially since the state or large exporters dominate them. Default risks may be contained to just a few banks, but the banking sector’s long-running consolidation since 2014-2015 continues and if real incomes don’t rise much and disposable income falls or gets slammed by inflation, I’d start to worry more about the banking sector. Though its stability has been assured, smaller banks likelier to drive individual or commercial lending in the regions face higher risks than, say, Sber who, like western counterparts, will have an interest in lending by algorithm and cutting costs, including reducing its physical footprint which leads to more underbanking. More banks will fold up voluntarily this year too, worsening this trend.

Capital investment levels spiked up significantly in December alongside the bizarrely strong manufacturing data for the month, but demand for construction materials as well as imports both ticked downwards a bit. The increase in production, however, is not the best indicator for Russia’s growth path in 2021:

Title: Dynamics of the component index of investment activity, monthly avg. ex. seasonality

Orange = production of cars/equipment and machinery for the domestic market Blue = demand (production + imports) for construction materials Seafoam = Imports of cars/equipment and machinery

Most of the spike in output can readily be explained by factories closing out orders from before COVID or the early stages of the pandemic as well as the impact of final budget disbursals since spending in Russia and procurement contract orders are almost always backloaded towards 4Q even in a normal year. Crucially, the underlying import trend for machinery and related inputs in 2020 was still one of growth, and the increase in 3Q-4Q corresponds to China’s rising current account surplus last year. Despite the rosier projections for a recovery in investment levels (which largely track with disposable incomes) — consensus forecasts seem to place GDP growth for 2021 at 2.9% as of now — the rise in imports vs. 2019 may stick a bit longer since Chinese manufacturers are going full bore already and the current oil price recovery will support Russia’s biggest exporters importing tech, but not a significant increase in construction demand. The consensus recovery forecasts seem in the ballpark for now, but topline GDP tells you nothing about the composition of growth. On that front, the skew in the late 2020 production data suggests, to me, stagnation sooner rather than later since back orders have been largely cleared, disposable incomes remain lower, and even when OPEC+ cuts are unwound, the corresponding drop in oil prices will start to weigh on demand under $55-60 a barrel.

Remember that story yesterday about the rise in Russia’s non-resource, non-energy exports? Well it turns out that gold exports account for the entirety of the increase (setting aside price inflation for food commodity exports, namely wheat). Over last summer into fall when the pathetic dysfunction of the US Congress and the presidential campaigns immobilized any deal for want of actually helping people instead of playing politics with the public’s lives, gold enjoyed a bull run while Russian production increased massively from 123 tons to 320 tons. The dollar value of exports rose by 320% year-on-year for 2020 to $18.5 billion. The UK bought over 91% of that trying to keep the GBP from sagging given just how dependent the UK is on imports of goods. Agricultural exports reached $30 billion in value last year. So really, about 30% of Russia’s non-resource, non-energy exports are actually commodities, one of which — gold — keeps falling in value this year as recovery in the US looks stronger and people aren’t running for cover from the US dollar anymore and other main one — wheat — is facing worsening export quota and tariff rules to try and keep more production on the domestic market and push more price inflation onto global market prices. The devaluation of the ruble will help around the margins for some exporters, but most of the gains come from commodities and low value-added production. At some point, the people peddling Russia as having weaned itself from oil have to grapple with the fact that it’s mostly boosted the sectors that propped up Tsarist Russia’s international trade and tax base prior to WWI, which isn’t exactly much of a growth driver in today’s world when it’s all cross-subsidized.

Total is expanding its partnership with Novatek (despite sanctions) and now investing into a new natural gas field in the Yamal-Nenets Autonomous Region that will help supply Arctic LNG 2, Novatek’s flagship expansion project building on top of the success of Yamal LNG. The Chernichnoye field is near another already in operation, hence the infrastructure costs to stand up production aren’t exorbitant. The details of the joint venture and the field aren’t terribly relevant. The important signal is that Total has no intention of stopping its natural gas investments wholesale and still wants a bigger piece of the LNG action in Russia’s Arctic despite any commitments to reduce emissions and shift its investment portfolio towards green energy over time. For Novatek, Total is a crucial bridge to protect itself from further sanctions in the West. I think it’s a foolish bet given that Paris has very little effective say in what the US Congress or Biden do in the end, though it certainly can lobby on Total’s behalf. But I’d wager that Novatek’s LNG is safer in Russia than Gazprom because LNG markets have finally gotten close to integrating regional markets. Price arbitrage, premiums, and discounts remain, but price levels across major regional basins — excepting shocks like a major cold snap — basically track in line with each other, which means that LNG contracts can more readily link prices between regions (but also has encouraged more oil-indexed pricing for market stability). The West wants to see that stick, especially since it further undermines Gazprom’s ability to set marginal prices as its own pipeline exports to China have actually reduced its negotiating power over prices with European consumers rather than increased it for precisely this structural reason.

COVID Status Report

In a slight uptick, there were 13,447 new cases recorded yesterday along with 480 deaths. The data seems unmoored from what’s going on still, and that’s reinforced by the announcement that Moscow clinics are rolling out “Sputnik Light", basically offering people partial immunity instead of full protection using a single-dose with benefits appearing within a week of vaccination. The case load once again doesn’t match what’s going on:

Red = Russia Blue = Russia w/o Moscow Black = Moscow

If they’re really so desperate as to offer partial immunity to speed up vaccination efforts by altering the Sputnik-V vaccine slightly, then it suggests that the Kremlin is in a bind meeting vaccination targets. Either the government wants the use Sputnik Light to help countries with high infection rates waiting on help from the West that’s not forthcoming, thus saving more Sputnik-V production for domestic use. Or else they want to use Sputnik Light domestically to speed up the re-opening and, without acknowledging it, be able to export more Sputnik-V since they’ve been trying to close supply contracts without any evidence that domestic production is adequate to maintain a good vaccination pace. The mortality data in 2021 is almost certainly going to expose this, but it’ll only come out after the September Duma elections have already passed. Speaking of which, the systemic opposition are pushing back against proposed expansions of single-mandate seats in the Duma at the expense of party lists. This vaccination and re-opening saga could become a political football later this year as they jockey to keep their influence.

Li in State

The OIES has a great, short report out on the geopolitical considerations of the energy transition, particularly focused on lithium and batteries. It well captures the geopolitical reality that China’s far ahead on the supply chain side when it comes to the intermediate parts we need for production of electric vehicles, home batteries, and the array of innovations expected to shake up the transport sector:

It’s exceptionally difficult to simply relocate a supply chain once firms have built up knowledge and practices, established themselves on a market with a more attractive exporting exchange rate, and so on. Even with Biden’s administration keen to leapfrog forward on electric vehicles, Europe remains the “swing consumers and producer” accounting for the balance of the global market outside of China for now. What’s crucial to acknowledge, however, is that the types of scale traditional internal combustion engine manufacturers were able to achieve is probably at least a decade away as companies scramble to reconfigure existing plants or else build new plants and establish new supply chains drawing on metal & mineral inputs from newer sources.

The US remains a ways behind, and the Trumpian turn on trade is going to stay, even if it’s executed and expressed differently. For instance, SK Innovation, a Korean battery producer that opened a $1.1 billion plant in Georgia, has been hit by an import ban for any components found to be using intellectual property from LG Chem, another Korean chemicals company thanks to a decision from the US government’s International Trade Commission (ITC). Though some existing supply contracts were grandfathered in, the ban would force the company to massive spend on R&D to replace the IP it lost or else find a new partner firm if it wants to maintain its US market share. These types of trade fights may end up re-shoring more production unintentionally depending on what industrial policies are offered up in Washington. They equally may just end up hamstringing the transition while competitors try and establish the type of global scale the previous generations of auto manufacturers achieved after the massive over-valuation of the US dollar in the late 70s and early 80s thanks to Paul Volcker’s monetary policy and then Reagan’s trade deficit and currency fights with Japan (and West Germany) that accelerated the globalization of production. We don’t know yet what to expect. Structural forces that may become more pronounced, durable trends suggest that Biden actually has an opening.

That’s where the relative balance of post-COVID recoveries get interesting — and also where Russia appears to be completely botching what would otherwise be an opening for political and economic engagement with the EU. Consider the Euro exchange rate against the US dollar. The higher it goes generally speaking, at least since the COVID crisis began, the greater the relative deflationary pressure/expectations are in the Eurozone vs. the United States:

After the initial rip down when Europe was hit first, the Euro has steadily appreciated against the dollar, which would normally correspond to an increase of imports and a decrease in exports over time. 2020 was odd insofar as the US stimulus package adopted early on massively increased spending power such that while the services trade didn’t vanish but was hindered from lockdowns and spillover effects of the oil price crash, goods were resilient. The US bought about three times more goods from the EU than services as of 2019 — roughly $450 billion vs. $145 billion — while the US ran a services trade surplus of about $54 billion for that year (but obviously a then relatively larger goods deficit given the overall trade deficit was worth $130 billion assuming we can trust the USTR data from Lighthizer). This doesn’t map perfectly onto the Eurozone obviously, but given the relative size of the Eurozone’s economies compared to non-members, it still captures the direction of travel for the currency fairly well. So on top of the deflationary risks in Europe affecting its own current account i.e. driving up its surplus, US exports to the EU are services-led and most likely took a harder hit. But China overtook the US as the EU’s largest trade partner in 2020 — turnover was worth $696.4 billion while turnover with the US fell to $671 billion. The Euro’s trajectory against the yuan differs significantly than that of the US dollar, even if the % changes are comparable:

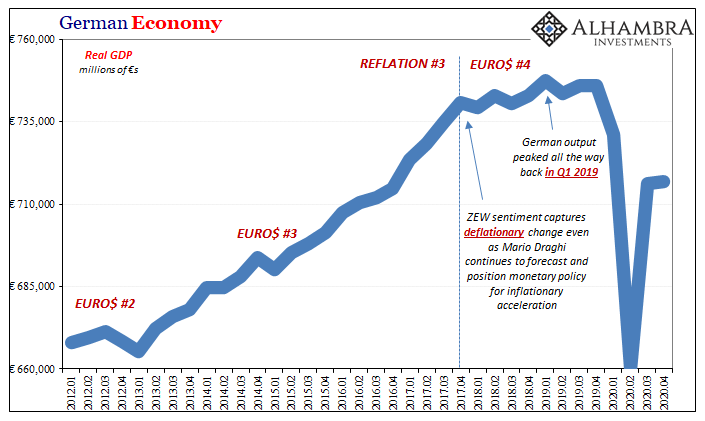

The Euro’s weakened against the yuan after an initial surge probably linked to a fall in imports before consumer demand adjusted and China’s supply side stimulus kicked in fully. These divergent dynamics also have a great deal to do with shifts in financial flows, financial accounts, and the money earned by European firms from investments in the US vs. what they’ve invested into in China i.e. companies have a lot more exposure to portfolio income in the US that isn’t tied to physical activity than China, but that will keep changing as China liberalizes capital controls and its financial sector further. China also actually received more foreign direct investment than the United States for 2020, but that won’t necessarily hold in 2021 given that US recovery appears stronger and stronger compared to Europe or analyst expectations. The divergent currency dynamics, however, create an interesting arbitrage opportunity for trade competitiveness assuming Europe’s troubles are only just starting. Remember that Germany’s woes began prior to COVID and despite Mario Draghi’s rise to power in Italy and renewed focus on recovery (which means a bigger likely fiscal stimulus), what happens in Germany is exported to the rest of the Eurozone:

A weak domestic recovery in Europe will leave its external exporters like Germany with a larger current account surplus, which will further strengthen the currency and erode their competitiveness at the same time the yuan is strengthening against the dollar. Yet the Euro seems to be on a downward trajectory against the yuan, which makes its exports into China more competitive over time. This is not yet a hidebound, ‘hard’ trend since it’s highly contingent, but that means that the US is in an odd position of having a slightly easier time on competitiveness grounds selling into the EU if it can create the right conditions for exporters to setup shop and handle trade negotiations with Brussels while also slowly having an easier time selling to China, or else moving production out of it. The yuan will inevitably strengthen given the growing pull Chinese consumers have on global markets and China’s export competitiveness into the US declines. These are long-term factors, but are crucial to understand when unpacking what the next stages of supply chain dislocation and relocation look like as the energy transition becomes more geopolitical.

Russia is completely absent from this part of the story, however. Everyone knows that the country has a terrible business climate, but large foreign firms are aware that the regime is able to promise major investments are protected. That’s always been the deal with foreign energy companies. Lavrov’s outburst about breaking ties with Europe, something that has been softened since, flies in the fact of an obvious opportunity to try and build trust by reaching out over the energy transition and, even more importantly, achieve some of the Kremlin’s standing economic goals. The biggest impediments are actually institutional more than political since Russia’s fiscal policy makes oil & gas a workhorse no matter if the country begins trying to take advantage of the energy transition, at least for the next decade. As of 2019, World Bank estimates showed it cost $580 for border compliance for exports from Russia vs. $256 in China, $345 in Germany, and just $175 in the US. Barries to border compliance can have positive externalities regarding quality etc., but in the Russian case, that cost is effectively just rents being extracted, whether by export duties and costs or by documentary rents whereby the Customs Service and FSB can extort or bully people or run their own contraband operations or else by trying to use various measures including quotas to discourage the export of production to keep domestic prices low. The effect of all that policy capture, even with efforts such as the harmonization of product markings within the EAEU to ease internal trade, is that even if a foreign firm could be convinced to setup a factory to build intermediate components or parts of an EV supply chain with the blessing of the Kremlin, every shipment entails additional costs that are significantly higher than elsewhere — 126% higher than in China, for instance. So while currency movements marginally shift to reflect China’s growth as a global consumer and reshape state and corporate responses to the energy transition, Russia’s once again absent because instead of focusing on soft barriers, domestic subsidies and import substitution efforts are privileged.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).