Top of the Pops

Tesla’s taking advantage of being registered as an energy provider in the UK back in June by teaming up with Octopus Energy offering competitively lower electricity rates for homeowners who install its proprietary solar and PowerWall tech and even lower rates for Tesla owners who have a charging station installed at home. While GM is giving Tesla major headaches on the Chinese market by targeting an ultra-cost model ($5,000…), Tesla’s now begun shipping its Model 3 from Shanghai to European markets. With demand for its energy storage tech outstripping supply, it’s interesting to see how the company’s model - effectively mimicking a confusing web of start-ups that don’t pay out dividends - seems better suited to the massive risk-taking required to come out the other side of the COVID shock. Watch to see if other manufacturers diversify their offerings in the space i.e. go further into energy storage or power generation to vertically integrate offerings. The market’s going to look a lot more competitive in just a year’s time as the old school incumbents for the auto sector learn new tricks.

What’s going on?

The Fund for the Development of Internet Initiatives is lobbying tax preferences for domestic software to be softened, allowing domestic software providers with foreign beneficiaries i.e. subsidiary firms, foreign owners, etc. to receive the same VAT exemptions that Russian firms do in order to be compliant with WTO competition requirements. The current tax change proposed by Putin in June would reduce insurance contributions from IT companies to 7.6% and taxes on profits to 3% while making up the revenue shortfall by imposing VAT on foreign software (and not Russian-made software per the national register of IT firms). It’s a useful case of how the regime’s constant appeals to international law and rules actually makes a great deal of sense to business lobbies trying to prevent trade retaliation and concerned about future export opportunities - another national goal to consider.

Russia’s banking sector earned 92 billion rubles ($1.18 billion) on the USD strengthening and are riding on a 20% profit increase in September vs. August. Looks like the banking sector’s sitting on a quickly growing pile of assets:

Title: Bank sector assets in 2020, trln ruble

You can clearly see the growth of the credit bubble since June. As in the US, those in debt are prioritizing paying back their debts whenever they can afford it, so its fat times for the big lenders but that quickly becomes a systemic risk in the event that incomes fall further.

The maturity length for credit extended to borrowers in Russia is rising, with the latest data showing the average loan is paid out over 43 months vs. 38 months a year ago. This fits in with the 33.2% of business and related organizations that are now unprofitable, a measly 3.2% increase year-on-year which suggests either A) the data isn’t terribly reliable B) support schemes for SMEs over the summer worked, but are ending C) a 3.2% increase is leading indicator of much worse to come. Much more worrying is that the total volume of borrowing hit 1.35 trillion rubles ($17.3 billion) for 3Q, a whopping 59% increase in volume from 2Q while the number of consumer credits extended has declined by 25.7%. That’s a massive red flag, though Russians are used to them.

The head of Yakutia Wisen Nikolaev is requesting that the government limit the projects that receive the status of a “regional investment project” (the aptly acronynmed RIP), a designation that offers severance tax and profit tax exemptions, because Far East regions are losing up to 33 billion rubles ($423.4 million) in revenues every year. The designation was written into a law specifically concerning gold mining operations offering tax breaks, an odd notion given the ostensible budget crisis and tax burden increases for other extractive industries. A large lobby clearly wants to increase gold output, which is probably linked to concerns about Russia’s de-dollarization and ability to sell gold to foreign central banks and investors. The tax code helpfully doesn't allow the retroactive cancellation of benefits.

COVID Status Report

Russia hit a new record for the 27th of October with 346 reported deaths from COVID. It’s striking to see an obvious and growing gap between the Rosstat figures and data gathered by the government’s operational staff supposedly handling the crisis response. These are reported deaths by month for April to August:

Top = deaths by month of those diagnosed with COVID-19 per Rosstat data

Middle = deaths by month of those for whom COVID-19 was the main cause of death

Bottom = deaths by month per government operational staff’s data

Given the rate of increase in infections, even a declining growth rate will lead to bigger and bigger absolute numbers across the country with no end in sight. Novaya Gazeta’s breakdown of the latest from across the country is damning as it’s clear that hospitals are again starting to be overwhelmed, if unevenly by region. It’s increasingly difficult to imagine this won’t derail the economic recovery, especially given the incoming lockdown regimes in Europe shattering the illusion that Europe had “figured it out” that held sway over the summer.

Balancing Without a Net (Zero)

South Korea’s the latest to join the club in Asia now that president Moon Jae-in has declared a target to achieve carbon neutrality by 2050. With Japan setting a 2050 target with Shuga’s announcement 2 days ago and the ongoing rumination as to the significance of China’s 2060 target, the US looks more and more the laggard. For Russia, that’s a big ****ing deal of great consequence, some obvious and some not. Though it’s not groundbreaking, it’s worth quickly pulling visualizations for the state of emissions with the relevant parties and some others as reference, including the US, EU, India, and Russia. Granted, the data’s a little old but still helpful and without proper adjustments for scope 2 emissions embedded into the goods trade:

South Korea and Japan are barely going to dent the problem, but have considerable power to affect carbon neutrality practices across supply chains in the Asia-Pacific. That could come to matter for Russia’s oil & gas sector, shipbuilding, and a few other industries, but not necessarily via the same mechanism as an EU-driven carbon adjustment system. Rather you could see either temporary gains for dirtier Russian manufacturers only serving the domestic market or, conversely, pressure to adapt carbon neutral technologies and practices because of import reliance. This year, the oil & gas sector had an import substitution target of 43% for the equipment it usually imports from the West. In practical terms, that’s a very slow rate of change since 2014 when sanctions first hit (import dependence levels were between 70-80%) but does represent progress. However, it’s not inconceivable that the manufacturers in China, South Korea, and Japan that have plugged the gap left by sanctions on European and US service providers offering up key tech and support, particularly for Arctic projects, can shape Russian firms’ attempts to replace tech through the diffusion of standards. Once Russian firms are used to working with x piece of tech, they’ll want to replicate its capabilities and functionality without losing any quality if they’re being pressured via policy inducements and subsidies to buy Russian-made kit. Particularly as concerns the efficiency of recovery rates - lower in Russia on average than for a lot of the sector in the US, North Sea, and Saudi Arabia - you want the best to avoid having to deploy capital much less efficiently over the lifetime of an oilfield. If the best tech is also the cleanest, Russian manufacturers will have to try and keep pace.

Japan and South Korea’s commitment are an opportunity to diffuse their own efforts to other economies in the Asia-Pacific that otherwise were the engine lifting oil demand growth the past 2 decades. Japanese firms have traditionally sought to maintain so-called China+1 supply chains: they would center production in China but maintain flexibility with an additional market to reduce political risks and enhance their bargaining leverage. Now that Shuga is doubling down on a subsidies policy to further diversifying supply chains - he’s made sure to visit Vietnam and Indonesia while talking up ASEAN’s potential to reduce its own reliance on Chinese firms and demand - corporate practices in Japan pertaining to carbon neutrality policies can be a useful touchpoint to influence policy in countries for which, until recently, Japan was happy to finance the construction of coal plants and more. South Korea just inked a trade agreement with Indonesia designed to improve market access for Indonesian exporters and expand South Korean investment into resource industries and business in Indonesia. Changes in corporate policies or lending requirements to finance said investments by setting carbon neutrality will similarly create policy pressure within ASEAN to push things along.

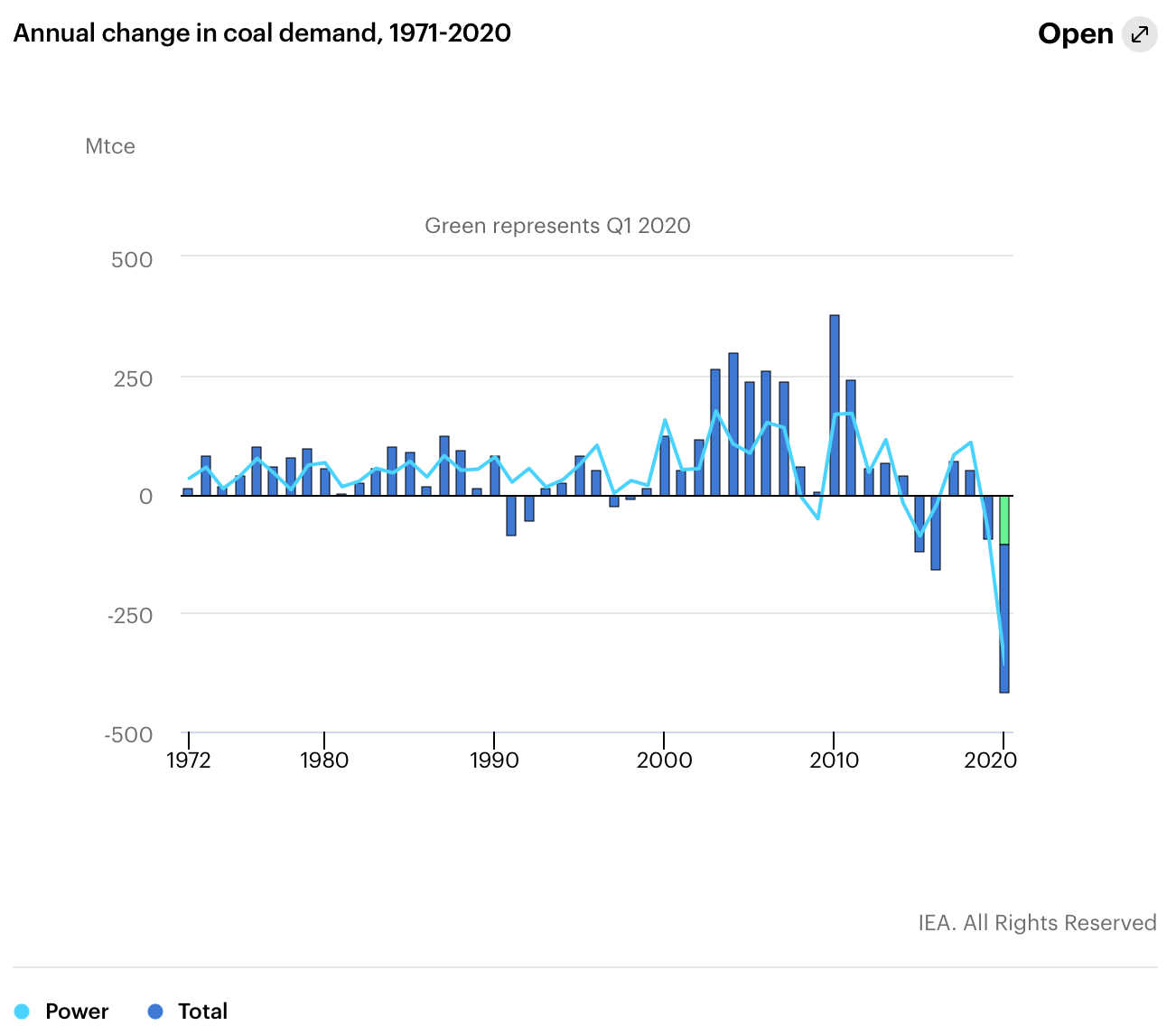

That should worry Russia’s coal sector, both for thermal coal demand and for maintaining competitiveness if these types of agreements begin to affect industry best practices and shape broader investment preferences. Coal demand isn’t going anywhere fast, but there is bound to be a fast correction on the power side. From the IEA:

The Pivot to Asia has always been a bit stillborn given how atrocious the business climate in the Far East is for foreign investors, weak infrastructure investment from the Russian government, and a general illiteracy when it comes to integrating the Far East into Asian supply chains. Sanctions weren’t stopping that investment from coming after 2014. Rather it was reticence from South Korean and Japanese business. Now that they find themselves having to scramble to handle China’s regional rise and a wholly incoherent US trade policy, they have a chance to accelerate aspects of the energy transition in the economies that have lifted oil demand and oil prices practically since 1991. Between about 1990 and 2019, Asia-Pacific consumers accounted for two-thirds of global oil demand increases, with another big chunk going to Middle Eastern consumers in oil exporting states whose consumption was jumpstarted by oil windfalls. Imagine what happens if South Korean and Japanese mileage and emissions regulations are diffused among car manufacturers trying to stay competitive in Southeast Asia?

This dynamic also points to potential to mirror some soft power practices - and impediments - for Russian firms trying to become first movers on carbon neutrality on markets in Eurasia if they see an opening. Soft power is often a wishy-washy analytical category to make sense of geopolitical and market trends, but this caught my eye when looking into ASEAN-Africa trade briefly thinking of Adam Tooze’s crucial point that the future of emissions reductions has to come from “the rest,” the economies of the world that aren’t China, the EU, US, or India. This graph from a July piece put out by Brookings on the role of family-owned businesses in Southeast Asia vs. Africa:

Convincing those business leaders to buy in is the next step and challenge. Russia’s traditionally relied on elite networks in Eastern Europe, Central Asia, and the Caucasus to maintain its political influence. This channel for diffusion is going to become more and more important if other large trade partners and sources of rents across Eurasia realize there’s a lot of money to be had in pursuing some kind of a Green Deal.

The Sold Coast Shuffle

Siluanov came out with a number putting Russia’s stimulus plans for COVID at 9% of GDP. It’s a bit ridiculous when you dig into the sums given that back in May, he was including not cutting the budget as stimulus, akin in some respects to telling someone you’ve just mugged that they’ve gotten great support from you since you didn’t take more. Alas, oil and equities are getting slammed now as investors realize that when France, Germany, Spain, and Ireland all put new lockdown measures in place and oil inventories in the US rise unexpectedly, maybe things are really, really, really bad. Siluanov’s problem is the same as that facing Rosneft and other commodity producers in Russia: external demand is slipping and dragging the economy down. But the clear policy preference in Moscow is to let lots of Russians die because they can’t afford to shut down the economy. Bad news for the Budgeteer: things are looking really, really, really bad at home too. From the CBR’s latest October release on inflation expectations:

Title: Expected and observe inflation by subgrouping of correspondents, median, %

Red solid = expected inflation (withs savings) Red dotted = observed inflation (with savings) Beige solid = expected inflation (with savings) Beige dotted = observed inflation (without savings)

Observed inflation with savings is matching expectations, and running weaker without them. Inflation is moving towards deflation, as we’ve seen, but it’s still pretty high given that incomes are falling and is being observed among producers despite the recovery in imports against fairly weak manufacturing recovery domestically.

Igor Sechin thinks he can message his way out of this dead end by decrying that China’s model for combating the virus has worked - never mind that Russia is decidedly not trying it out - but also that it’s driving recovery. Irony of course being that China’s recovery is not the Asia-Pacific or Africa or literally anyone else’s gain. His presentation at the Eurasian Energy Forum in Verona mirrors what’s becoming the language of decline for Russian elites. Hold up China against the US as an alternative model, say a bit about lack of investment into hydrocarbons bringing great wealth to Russia, smile, nod, assure oneself that people still care and the market jitters at whatever you do. Reality is different. Just as changes in South Korea and Japan’s carbon neutrality stances can spillover into ASEAN, they have some semblance of an understanding that from ASEAN, they can nudge “the rest.” Russian policymakers seem to have lost that vocabulary, that awareness of varieties of capitalism and carbon neutrality aren’t just about the “great powers.” The middleweights do a lot of the heavy lifting when it comes to normative shifts.

If Siluanov’s continued hawkery hinges on a price rally in 2021, then the economists in Moscow have simply stopped reaching for answers. It’s too bad Medvedev’s a punching bag now. He at least feigned interest in cultivating an economic relationship with African nations and “the rest.” Inflation and macro indicators are going to be bad for as long as the pandemic stymies global demand. Russian policy comes first as tragedy, then as farce, then as tragedy again on repeat.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).