Top of the Pops

Russian refiners are asking for additional budget support via the (infamous) ‘damping’ mechanisms that compensate refiners for earnings losses when lower oil prices crimp product margins (worsened by the oil price’s feedback into consumer demand in Russia, not just the pandemic’s effects). Now that refiners are trying to hold wholesale fuel prices down, it’s costing them more and they’d like more help. This year’s indexation for the mechanism was capped at 5% as of January 1, a sum inadequate to the price inflation seen since. For reference, it cost the Russian budget 400 billion rubles ($5.25 billion) to subsidize refiner earnings. This transfer to refiners has been locked in by the gradual elimination of export duties on crude to be replaced with higher mineral extraction taxes, making no difference to vertically-integrated companies but affecting refinery costs, fuel volumes not produced, refined, and traded through said companies, and the base feedstock cost more broadly. Instead of allowing price increases to encourage efficiency gains and finance refinery improvements, the budget is paying back a chunk of the revenues its raising off the sector.

The issue of rent and rent distribution is a pressing issue, but one that appears to get short shrift in the presidential administration and cabinet even with Alexander Novak’s elevation. MinEnergo calculations posit that only 36% of Russia’s remaining 30 billion tons of oil reserves are profitable to extract in the current macroeconomic climate. If one assumes no net gains from technology (unlikely) and a daily production rate closer to the pre-COVID levels of 11 million barrels per day, Russia’s got something like 20-25 years of profitable oil left (assuming present conditions). The trouble is, of course, that it’s difficult for technological advances to make that big an impact on profitability for the biggest reserves left since they tend to be increasingly remote, harder to recover, or else in the Arctic. Much of this can be ameliorated, but not totally overcome. That calculation is a tenuous one, don’t get me wrong, but it captures the problem. You can’t wait to pivot economically 5 years from now. It has to happen now. Immediately. Attempts to do so since 2013 have failed, not for lack of effort or options, but because of a refusal to let market prices or firm failures function without significant distortions that preserve employment and stability at the expense of competitiveness and institutional reform. Everyone’s hoping Biden’s policies support short-term oil demand. But with an effective planning window in Moscow that’s less than two decades and the growing problem, already present via tax breaks for Rosneft and old fields, of foregoing oil rents to sustain oil rents, the short-term matters less. Yes, we may be dead in the long-term, but markets still set prices and make investments with the hope that we’ll live awhile into it.

What’s going on?

In response to what’s expected to be a more complicated market for LNG in the next 15 years, MinEnergo is calling for a new program of state support for LNG projects to increase LNG’s total annual production to 140 million tons (around 190 bcm) bay 2035. Net production was 30.5 million tons (41.5 bcm) last year. The proposal is straightforward: the state picks up the tab for new infrastructure and provides guaranteed cheap credit for existing and new projects, and using long-term supply contracts, presumably negotiated by the state with the company, to ensure adequate revenues. The entire program of support, however, is coming about because they no longer expect demand for LNG to grow as much as they did pre-COVID. But American equipment accounts for over 90% of the gear used in large-scale LNG projects in Russia, which creates huge import substitution pressure, especially with any shifts in sanctions. So state support also has to concern industrial policy. Coming expansions of capacity like Novatek’s Arctic-2 LNG will push Russia towards or else into the top-3 global LNG producers but its current production target would be optimistic even with strong demand. Seems that Moscow’s now going to have to throw more money at LNG to keep its competitiveness up, which could cost not just more budget resources, but opportunities as well depending on decarbonization pathways in importing economies in the next decade.

New data confirms the fears of the CBR from over the course of the last year — the amount of cash rubles in circulation has hit record highs. Despite the growing popularity of electronic payments, Russians wanted cash to get through lockdowns and restrictions:

Title: Dynamics of rubles in cash circulation

Yellow-Green = blns rubles Red = % year-on-year

The rise in cash spending and hoarding logically corresponds to the higher inflation pressures the economy saw with some consumer staples starting in 3Q, even if it’s not likely a major driver. The more of that money flows into the informal economy — much likelier when employment figures overstate the recovery and more people are forced to take on extra work where they can, especially if they’re trying to save enough to exploit the mortgage subsidy scheme — the more inflation creeps into consumption through measures indirectly. A combination of a lack of faith in the banks and delayed demand i.e. people withdrawing cash for future consumption when things settle down explains a lot of the surge, as does the drop in the key rate for deposits to just above the inflation target.

MinFin has put forward proposed changes to the state procurements system to the Duma and frankly, they look terrible for competitiveness. First, the good. MinFin wants to completely digitalize the process and system, which saves everyone time, paperwork, and headaches. It also makes it that much easier to use informal means to ‘win’ contracts since it cuts out physical stages of the process and people to worry about. The processes by which contracts are awarded are also being simplified to an auction process, competitive bid, or else the use of quotas provided for pricing etc. But after that, attempted modifications to the rules meant to expand access to contracts for SMEs are actually going to hurt them — companies bidding on contracts over 20 million rubles ($262,465) have to show they’ve had past experience/success with such contracts. It’s basically a grandfather clause ensuring a shrinking circle of firms win bids. Plus they’re no longer publishing who wins contracts publicly to reduce sanctions exposure, but that means there’s even less transparency (if that was possible) and smaller companies will struggle to figure out who actually won X contract. MinFin is killing the best means of cost control it has — public shame — and getting little in return.

The creation of the state firm Tourism.RF was part of a policy drive to increase Russia’s tourism exports as part of a broader economic rebalancing, but it looks like fiscal consolidation is undercutting those plans. Initial plans called for 432 billion rubles ($5.67 billion) of state support to build up tourism infrastructure, but reports now suggest that while businesses are keen, the government is less so. It’s expected that net earnings from foreign tourism will more than double by 2030, but the real driver for growth is an expected 220% increase in domestic tourism. This growth is expected to create 2.2 million jobs over the course of the next decade, though one wonders how exactly this is supposed to work with demographic trends and the underlying reality that productivity gains are slow across the broader economy and there’s limited evidence higher-productivity, higher-wage jobs are appearing in adequate numbers given that average real incomes continue to stagnate or decline. Business interest isn't a reflection of getting a state handout, I think. Rather it’s evidence of suppressed supply for services that Russians want access to. Now’s the time to make investments if Moscow really is so confident that its vaccination strategy will revive the economy.

COVID Status Report

Cases ticked back above 19,000 and recorded deaths stood at 575. We can finally see a broader decline in the intensity of the number of people infected per the Operational Staff’s figures:

A few people in Moscow are undoubtedly patting themselves on the back now that UN General Secretary António Guterres has said Russia’s vaccine has an important role to play in combatting COVID, pending the WHO’s certification for which he stated talks are now underway. That’ll help vaccine diplomacy’s legitimacy, if not the problem of production and distribution. Regional governments are beginning to make preparations for elections and related processes to still be affected by the virus, even with vaccinations now climbing. The regional parliament in Krasnodarsky Krai — notably the in the worst affected zone in Southern European Russia — has passed a law extending the voting window for regional elections to 3 days. Others are less concerned about the virus, but still laying groundwork. Novosibirsk governor Andrei Travnikov is already assuring everyone the campaign season will be respectful and not ‘excessive’ (whatever that really means here). It’s campaign season till September. All policy moves concerning the virus from here on out should be seen through that lens as vaccinations are doled out and national conditions appear to improve.

Out Transit

Reporting from Kommersant on research from InfraOne shows that the infrastructure sector of the Russian economy took losses exceeding 1.9 trillion rubles ($24.9 billion) in 2020. The data charts out how much earnings dropped off and shows the initial gut punch to transport infrastructure, which then eased as restrictions were cut and relaxed:

Title: Net decline (growth) of sector earnings from COVID-19 (blns rubles)

Blue = transport Black = utilities Beige = energy Orange-Red = Social

Transport’s clearly the sector that’s taken it most on the chin. Average declines in earnings for airlines reached about 42-43%. Airlines and airports lost a combined 713 billion rubles ($9.35 billion) while RZhD and the rail sector lost 144.3 billion rubles ($1.9 billion) mainly to the massive drop in passenger fares. These declines in earnings reflect, partially, the influence of price control policies as well. The Federal Anti-Monopoly Service (FAS) seized control of airline ticket pricing when the pandemic first hit to prevent airlines from using domestic price increases to offset losses on international flights, a smart policy choice given that infection rates would likely have proven higher on trains carrying passengers over long distances and also royally screwed Russians living far away from their families but still one that distorts slightly the picture we have of how COVID hit infrastructure earnings.

What’s curious here is that if an economy has the fiscal capacity to borrow cheaply or else lots of reserves in hand, rising revenue capacities to finance spending, a very low level of external debt, and a systemic infrastructure shortage that generates seasonal cycles of bottlenecks and related problems, then a big infrastructure program is the perfect stimulus. It increases domestic intermediate demand, creates jobs, reduces transaction costs for domestic businesses, eases travel, lowers logistics costs, and more. So where’s the program in Moscow?

On January 13, Putin made it publicly clear that infrastructure development should be a priority:

“We should give [our] attention to the development of infrastructure generally. I don’t only mean road construction, but railway construction, and the development of pipeline transport.”

First of all, there’s a definitional problem. Infrastructure in Moscow policy speak can cover any number of things that aren’t expressly for the purpose of communication across great (or not so great) distances. Last September, a trillion rubles ($13.1 billion) was authorized for the development of infrastructure “in the sphere of ecology.” Suffice to say that while that might entail some green spending, it’s more likely a bunch of insider deals for stuff like municipal waste dressed with the word infrastructure thrown in to make it sound better. They even framed the bill in terms of meeting their Paris Agreement obligations, which we all know are set against Soviet emissions and thus a sham. I pulled the spending program figures provided from RZhD for 2015-2019 (2020 is still missing) and they suggest something interesting:

Most of the spending increase can be chalked up to the ruble’s devaluation, so this isn't proof that RZhD launched a more expansive program. But consider what they’re spending on and the timing. The biggest line item from the state mandated project list spend for 2019 was the Moscow Transport Hub, which is great if you want to make sure Moscow has easy access to import yet more stuff with its excess earnings, but not that particularly helpful if you want to make other parts of the country not only more competitive, but a better destination for foreign investment in the future in hopes of exporting to China. Instead, the biggest spend there (rationally) is on the Baikal-Amur Mainline and breaking up bottlenecks on the Trans-Siberian route. And this doesn’t count the massive waste of federal money on Arctic rail (not necessarily spent via RZhD) serving regions that deserve support but have become an economic priority at the expense of sustainable growth elsewhere.

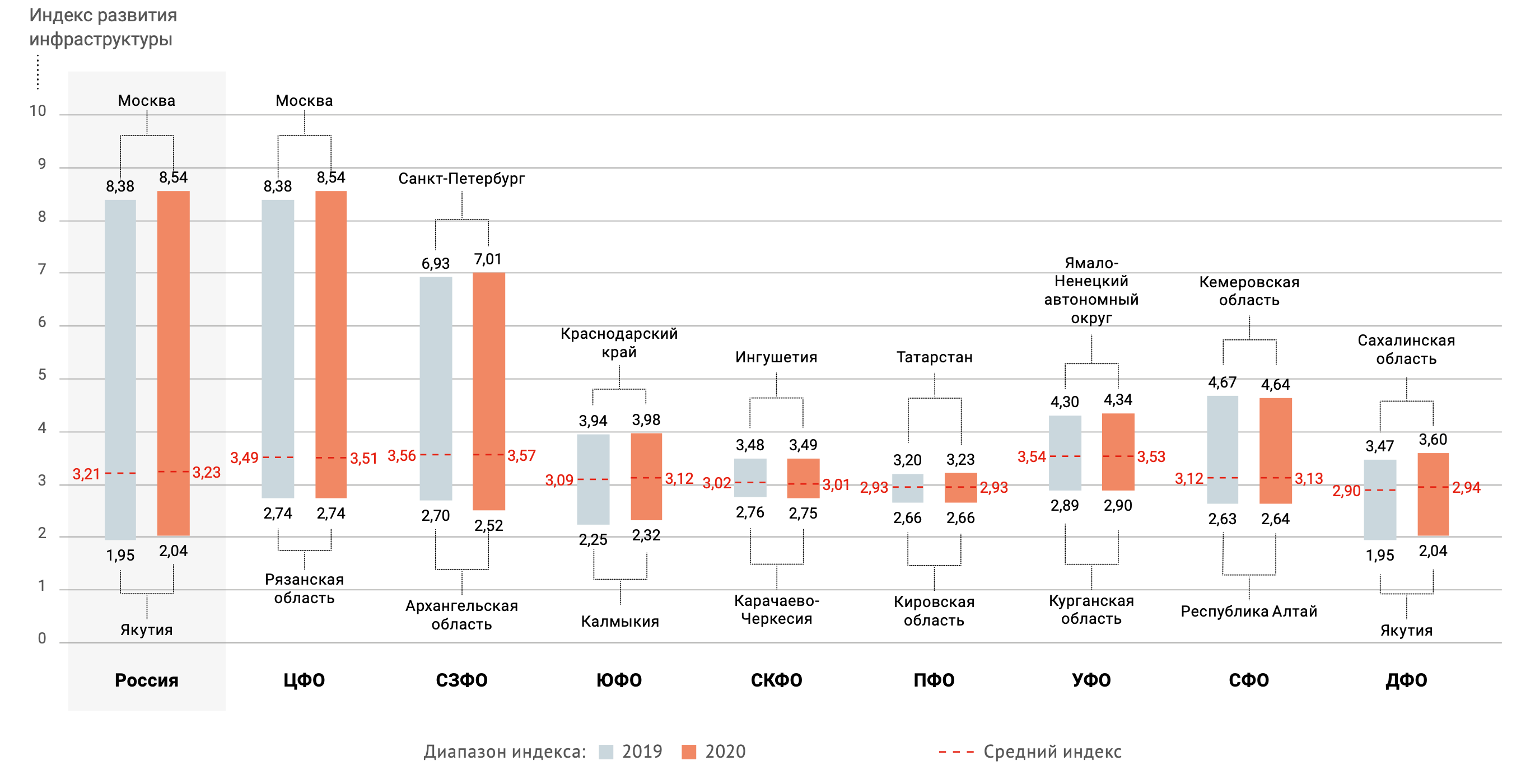

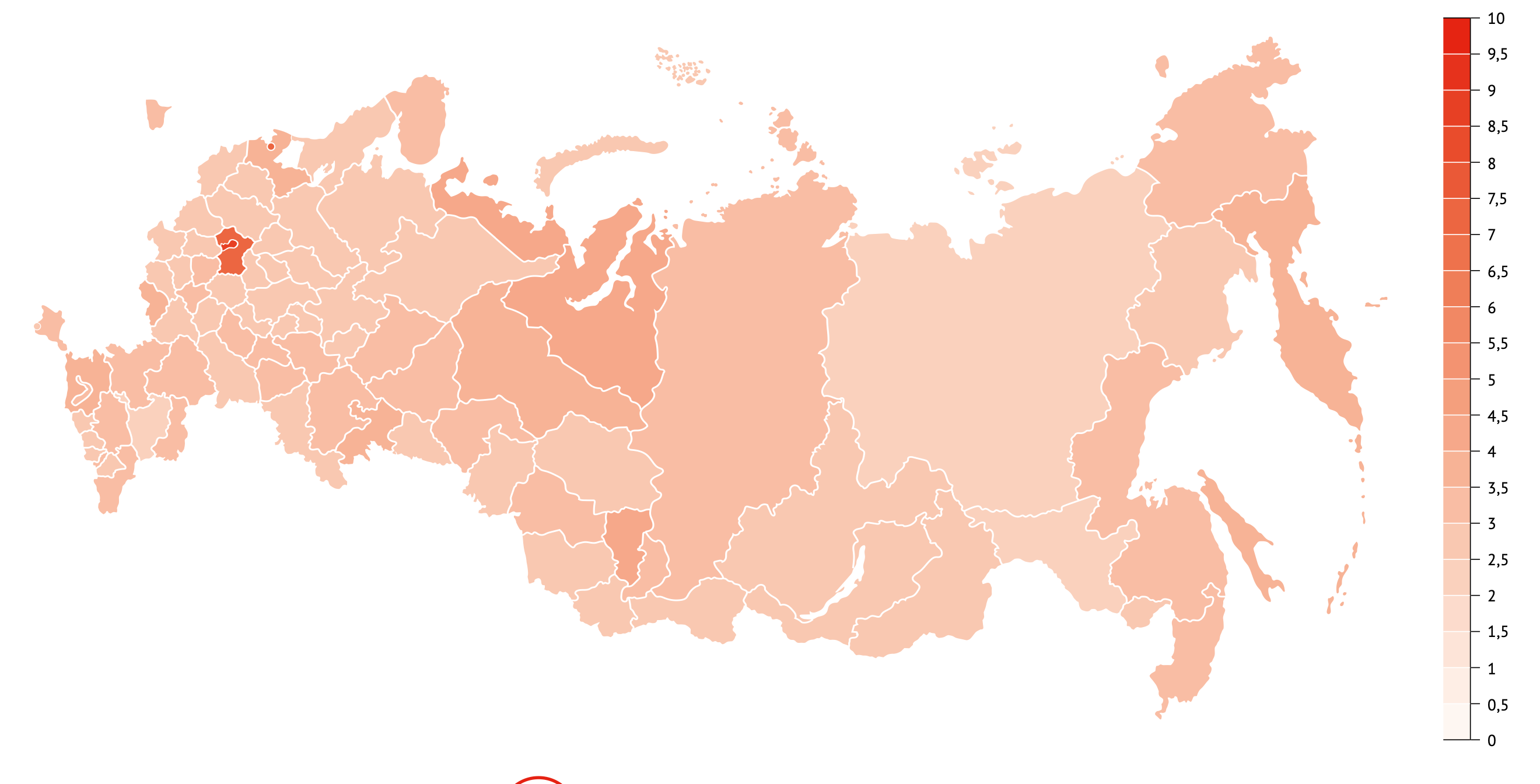

As we can see, spending for RZhD appears to be (slightly) increasing before COVID, partially as part of a ‘burst’ of works to capitalize on the rise of China’s rail export routes to Europe. However, these works were years late to best do so and Kazakhstan managed effectively to capture a great deal of those volumes and, crucially, the profits realized from building up transit capacity is greatly exaggerated. It’s most useful if you’re trying to develop new industries for export, otherwise you’re just making it easier for Russians to buy things made in China (which happened last year as we saw, aided no doubt by online orders). So that might be why Moscow’s been circumspect about announcing a big, new spending program. It’s moronic when you look at the data from InfraOne highlighting regional infrastructure disparities. I forewent translation just to save space:

As you can see here, Moscow and St. Petersburg are way ahead of the rest of the country. Krasnodar Krai should not be less than half as developed as Moscow when it’s the logistical gateway to Russia’s agricultural breadbasket. The extent of the gaps are truly worrying for the index measure:

It’s just Moscow that performs particularly well, with St. Petersburg and its port acting as a sort of ‘island’ in Leningrad oblast’. Back in 2017, Moscow accounted for 25% of the total national spending on infrastructure — 500 billion rubles for Moscow against 2 trillion nationally (I didn’t covert due to inflation and exchange rate fluctuations being more significant than for 2019 numbers). That dynamic is still the case given that an inordinately high % of the country’s imports are shipped to Moscow as a logistical hub before heading elsewhere, a centralization that imposes extra costs with little conceivable return but is buoyed by the high wages in and around Moscow given its huge share of GDP. And in actuality, projected 2019 infrastructure spending backed by the budget was expected to be a 6 year low at the time (this isn’t the same as RZhD’s budget, importantly).

So Russia was spending on infrastructure at the lowest rate since the economy entered stagnation in 2019 before COVID and with another economic slowdown that predated the oil price crash in 1Q 2020. It is exceedingly difficult to grasp how it is anyone can take Russian power seriously on the international stage (setting aside nukes and some cyber) when it can’t even be bothered to invest into the basic infrastructure precisely needed to fight domestic inflationary forces, promote balanced growth, and, I don’t know, actually move military units around when needed. China’s investments into high-speed rail were terribly uneconomic:

Pettis points to a basic problem with China’s HSR — pro-cyclical forecasting of economic returns neglects to mention that infrastructure spending is boosting expected growth i.e. it’s a circular reference. Building HSR creates today’s growth that’s cast forward, then justifying building more HSR. But what China got for it was the ability to move masses of troops around domestically in rapid fashion as well as providing fast transit for those who can afford it and a development success story to sell to western observers who rightly complain about the state of their own country’s infrastructure. The difference for Russia is that, despite the huge problems with its concessions law and legal regimes for PPPs and other infrastructure initiatives (something I used to dabble in and will happily opine about in the future), its working off a much lower base for growth and would see more substantive benefits because of the country’s systemic underinvestment in infrastructure.

China and Russia are opposites in this regard. Whereas China adopted a model of growth driven by over-investment into physical things like infrastructure, Russia’s shattered its growth by never investing enough. Without a new infrastructure program, a post-COVID recovery is going to lag and become oddly lopsided. Service providers like Sber will reap the whirlwind while brick and mortar businesses will face some constraints from a likely slight dip in an already precarious investment cycle that will also constrain potential demand. People don’t order things they know won’t arrive in time etc. The energy transition is an infrastructure development story. You’d think Russia would be interested in at least getting the basics right now when the fiscal multiplier of any spending will be higher and the bond market has shown there’s adequate domestic demand to finance a significant push. The 2019 shortfall in infrastructure spending was forecast at 2.6 trillion rubles ($34 billion). I can’t imagine that the 2020 figure is better, and it’s likelier worsening with the new budget measures. The problem with such shortfalls is that they accumulate, not only robbing the economy of growth and higher incomes but raising the cost of the bill when it comes due. It might be time to start thinking in those terms for economic policymakers, especially since infrastructure spends are great at buying votes. If you keep tightening your belt, you’ll eventually cut off circulation.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).