Top of the Pops

Armenian foreign minister Zohrab Mnatsakanyan reportedly told Russian FM Sergei Lavrov that the return of Armenians dislocated from Nagorno-Karabakh by the conflict to their homes was necessary, as were steps to protect their rights within the current settlement framework on a phone call this morning. The call is backgrounded by reports from US diplomats and military officials that Baku has granted Israel access to airfields on the Iranian border, a leak to Foreign Policy magazine (admittedly from 2012) suggests the US wants it known whose side it’s really on i.e. not to destabilize things further. It’s worth flagging that while quite an old report, it’s never been properly denied and Israeli media is now promoting Az-Israeli ties again. Basing rights represent a poke in the eye for Tehran, yet another reminder that Israel and Gulf states now embarking on large weapons purchasing programs from the US have effectively forced it into a position to feel threatened no matter who enters the Oval Office on Inauguration Day. As a result, Tehran is now faced with the difficult balancing act of maintaining its support for the current peace process while Baku provokes it. It’s another manner in which prescribing a Russian victory was quite premature — we’re only now beginning to see the knock-on effects and whatever the condominium in the South Caucasus be, it now is ensnared into broader problems in the Middle East between Turkey, the Gulf states (and Qatar), Iran, and US policy.

Petroleum Economist ran a piece noting the decline of threats of supply disruptions in the Strait of Hormuz, an old canard ascribed to Iranian strategic thought that, while strictly true, was never a logical priority or risk. But the piece somehow misses a fairly obvious piece of the puzzle in the last 2 years: it was actually companies like ADNOC from the UAE that first moved to build a new refinery and pipeline capacity for a port past the strait before Iran and other Gulf states mirrored its moves. The UAE’s now buying $23 billion of weapons, including F-35 stealth fighters, in what will be a further escalation of military tensions. You don’t buy hardware and park in ready to go just because you want to bluff or sleep better at bet. These policies are coordinated with Israel’s “winning the peace” in Nagorno-Karabakh and the United States new leak that Al Qaeda’s second-in-command was killed in Tehran in August. It’s time to start widening the aperture to make sense of the conflict’s fallout.

What’s going on?

Per a new draft law, the government is centralizing all state orders for construction into the hands of one special-purpose public company. The aim is to simplify the mechanisms by which such orders are made to improve the effectiveness of construction orders for the state’s Federal Targeted Investment Program (FAIP), the flexibility of contracting for these projects, and presumably to reduce potential waste by making oversight simpler. Since Oct. 1, MinStroi has already taken over construction contracts for four other ministries. But capital investments aren’t considered part of the project. Translation: we’re just fiddling around the edges to give MinStroi more negotiating power, but not touching the bigger sources of waste and inefficient expenditure.

Since the start of the year, regional social welfare authorities have entered into 85,000 support “contracts” — agreements with individuals drawing on social security budgets who fall under the federal poverty line. Nearly half come from the top 5 regions where people availed themselves of the programs. The causes correspond directly to COVID-19:

Gray = difficult life circumstances Black Shading = searching for work Red = professional education Dark Gray = starting a business

While a small population size all things considered, it’s telling if expected that around 87% of all claimants are struggling with their income. These are dedicated resources serving a vulnerable population, so one would expect clustered results. However, the Duma just took a bill for first reading that would raise the poverty line while also raising federal minimum wage. The problem, of of course, is that when you factor in wage arrears and current disruptions to steady work in the formal economy, they’re effectively preparing to cut off access to social support at current measures while trying to force firms to raise their labor costs. More people are going to fall through the cracks.

January-September sales of antibiotics in Russia rose 14% year-on-year, which begs the question what people are thinking. The sum is comparatively small — 28.6 billion rubles ($372 million) — and broader medicine sales rose 15% for the same period. Still, COVID is a virus, not a bacterial infection, and the increase in sales suggests a few possible things: people are getting sick more often, people are more worried about getting sick, people are buying antibiotics to treat things improperly, or people are being referred to buy antibiotics by doctors and other help in place of in-person treatment as hospitals and doctors’ offices manage infection caseloads. Much of this surge could be people developing bacterial infections as a complication from COVID, but I have a hard time believing it doesn’t correspond to straining medical care capacity. It goes to show that there are a chain of effects that aren’t always readily visible until later.

The State Legal Administration of the President (GPU) is expressing concerns about proposed reforms to bankruptcy laws put forward by MinEkonomrazvitiye meant to take effect next year. The aim is to allow companies to get through the rough patch of a bankruptcy allowing external administration to take place and aggressively fix finances. The most contested idea within the proposals is to make the Federal Tax Service a secured creditor during this process, legally possible per existing regulations but largely ineffective because of the conditions necessary to trigger the relevant legal clause. GPU members are concerned that changing the bankruptcy system as the moratorium on bankruptcies is lifted next year will end up increasing uncertainty and worsen outcomes for businesses rather than save them. Now that I live with a lawyer, that rings true in terms of the logistics, but it’s a sad state of affairs when Kremlin lawyers are trying to find to delay potential aid to SMEs and other companies most affected by COVID-19 rather than offering ideas as to how the ideas could be reasonably implemented on as fast a time schedule as possible

COVID Status Report

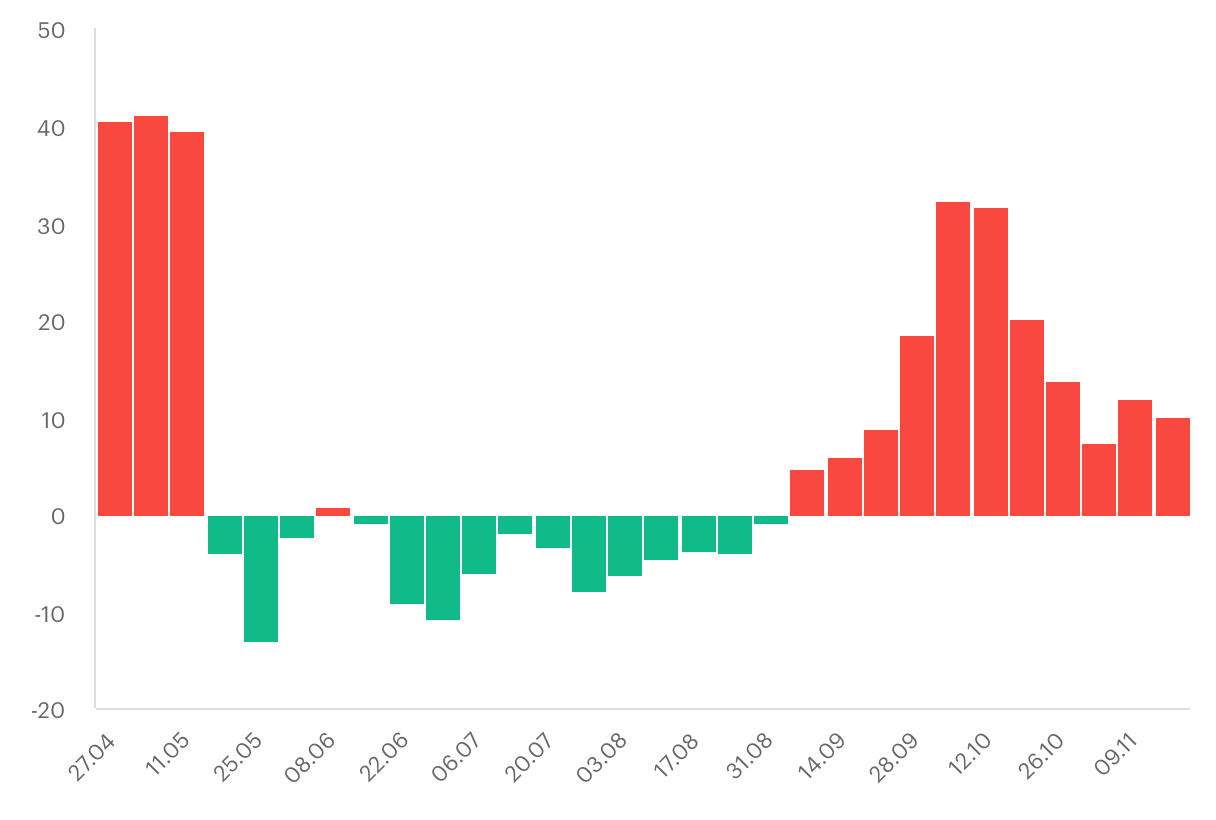

22,778 new cases have been reported for the last day and it looks like Buryatia’s going into semi-lockdown closing down non-essential stores and businesses. The success curtailing the spread in Moscow has barely dented the % growth rate in cases now seen with a growing absolute base. It’s still above 10% week-on-week:

Buryatia is the leading indicator, the first region to re-enter lockdown in response to rising infection rates. This cuts against everything Putin was messaging governors earlier in October. A lot of regional governments are going to be weighing their options very soon. Hopefully Moscow’s financial support keeps pace with what comes next. If it doesn’t, there’s going to be much greater strain in center-periphery relations.

Optimize Prime

I’ve been thinking more about the struggles facing Mishustin since he’s now the last hope for Putin when it comes to engineering some sort of stabilization and recovery for domestic economic struggles. The language of “optimization” has crept back into the discourse, the latest case being Mishustin’s commitment to cutting government employee rolls by 5% in central departments in Moscow and 10% in territorial organs. The idea is to do what the Republicans in the US like to: freeze new hires and let retirements, early or otherwise, chip away at the workforce organically. No one’s fired and forced out, no one’s actually happy, expertise inevitably gets lost but, in the Russian case, that’s just as likely to mean that newer hands less drawn to corrupt practices because of the new rules of the game get a shot at managing things. Mishustin’s applied the same messaging to reshuffling and clarifying responsibilities within his cabinet in order to better realize the national targets now delayed till 2030 in many cases.

Optimization is a curiously Russian approach to solving a systemic problem built into its political economy. The more central political power is weakened or slackened, the more peripheral political actors exploit the relative weakness of the center to dictate outcomes and the more difficult it becomes to mobilize resources in a state and economy facing chronic shortages of supply and/or demand. Optimization is bureaucratic speak for improving the administrative quality and efficiency of a system as it is rather than remaking that system as needed. It goes back over half a century to Soviet debates on reform initiated under Khrushchev. Khrushchev’s problem was reforming a grossly underperforming agricultural sector while managing the development of Soviet oil & gas reserves into a driver of economic growth and currency earnings to finance imports and budget shortfalls related to shortage or import inputs into the economy.

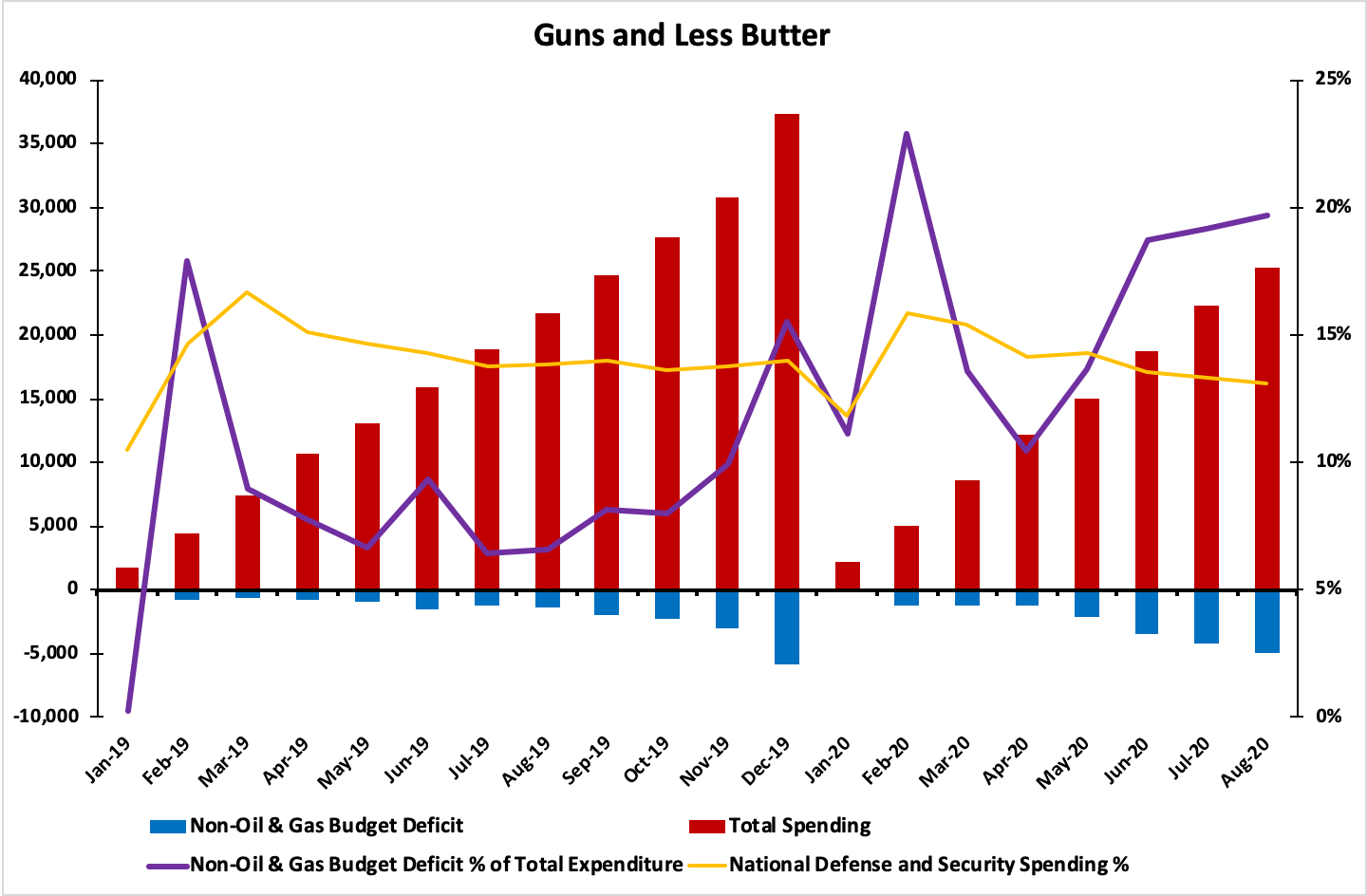

Mishustin’s picking up the ball further down the line. Agriculture is booming, in fact, but no matter how hard the state tries to reduce its oil dependence when it comes to its budget, the strong role the budget plays in guiding economic activity and the role of the oil price in the country’s business cycle and banking sector health make it quite difficult to escape dependence outright. Pulling Ministry of Finance data for 2019 through August this year, you get a snapshot of total spending levels vs. the projected non-oil & gas deficit within the budget, that deficit’s share of total expenditures, and as a reference, I included defense spending as a % of the budget. All figures in trillions of rubles:

The data is monthly so you’d expect it to build over the year, with any data in January and February being quite noisy since it’s rolling off the end of the prior fiscal and the budget tends to get spent more heavily in 3-4Q anyway as bureaucrats realize if they don’t use it, they’ll lose it. As we can see, defense spending shares of the budget are relatively stable, if declining some this year. I don't trust the topline figures as MinFin also classifies revenues from the oil & gas sector in such a way as to hide how important they are — Russian energy firms generate a large share of VAT receipts, for example — and there are considerable sources of cross-subsidization and spending that are effectively for defense not marked as defense. However, this is consolidated budget data, and hence not just federal and has its own peculiarities. As we can see from the COVID-19 shock this year, the non-oil & gas deficit within the budget skyrocketed with the demand shock in April-May at over twice 2019 levels.

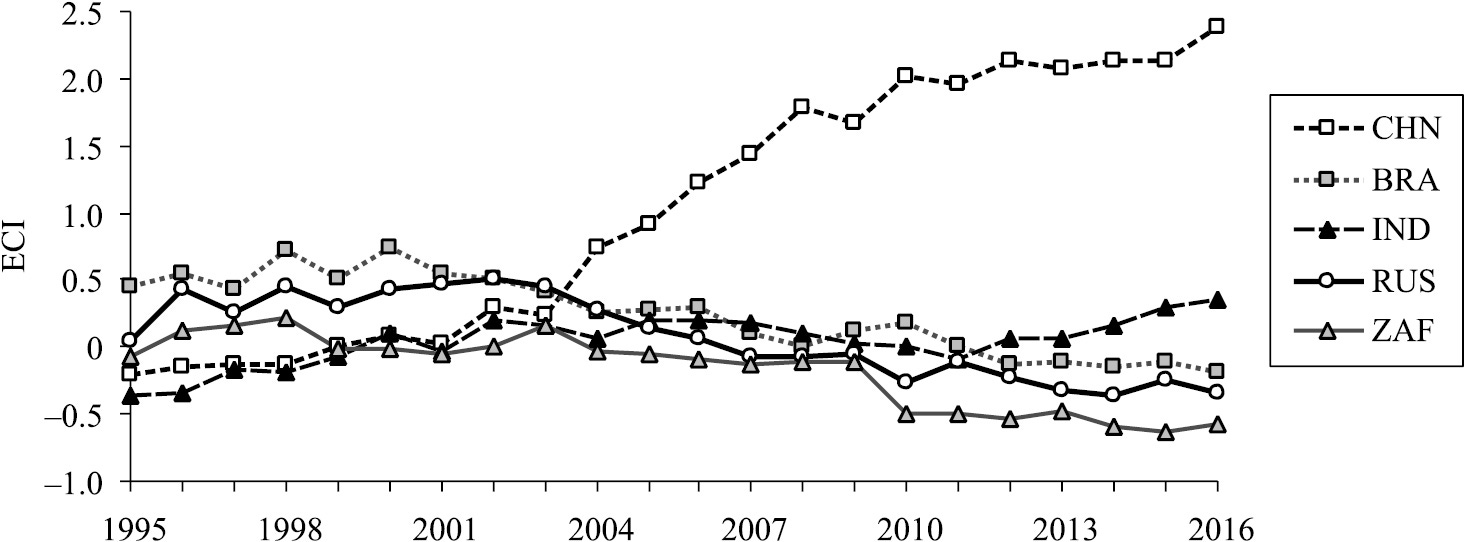

Optimization can’t fix a problem like declining oil & gas revenues. It’s solving a different problem, but one that is part of it. This data is dated now and has likely seen some improvement, but consider for a moment just how economically un-complex Russian exports were by 2016 compared to its own past:

In a best case scenario, Russian exports by this year were probably as complex as they were around the global financial crisis in 2008-2009. This is where the budget, oil dependence, and optimization all intersect. The commodity boom in the 2000s became a budget and foreign currency windfall which were then redistributed via social transfers and higher wages or else sterilized in rainy day funds designed to lower borrowing costs. Export complexity declined. Russians were importing more of the nicer goods they didn’t make themselves. That dynamic crawls to a halt in 2013 despite oil prices being higher than $100 a barrel. A healthy budget, low external debt, and excessive savings became a net drag on growth. Russian policymakers refused to spend at adequate levels, worried about sanctions and currency risks from 2014 on.

Now, every ruble not spent generating demand or investing into infrastructure and productive capacity to change the country’s production base for domestic consumers and try to capture elements of global value chains with trade partners is basically going to show up as a future deficit and yet more fiscal austerity. If you think about those % from the first chart, the net surplus for the budget corresponds to lost growth for the non-oil & gas sector since that money could be redistributed via social transfer or else put into projects that would enhance business competitiveness, reduce logistical costs, enhance commuter access in urban markets to help the services sector, etc. These numbers only go back to Jan. 2018 since I wanted to show figures after the oil market had stabilized and the banking crisis triggered in 2014-2015 had been unwound. Note that I had to smooth over quarterly growth figures into monthly data, and that they’re taken from the OECD for sake of ease this morning:

Oil rallies to the mid-80s per barrel in fall 2018, no movement for the net surplus of note while the non-oil & gas deficit surges, as it usually does, in 4Q. In 2019, prices are more often in the range of $58-65 a barrel. But we see a slowdown in growth that precedes COVID and no substantial improvement or change for the underlying trends for the non-oil & gas deficit, despite progress in some sectors. Then the oil price crash brings the entire budget into deficit by May-June, though when you consider the size of the previous net surpluses, it’s rather insane that fiscal consolidation was seen as the necessary policy antidote. The losses incurred by failing to spend I posit follow a fairly predictable Keyenesian logic: increases in investment correspond to increases in employment, which then correspond to increases in demand which then beget business profits and so on. But I’d add a twist.

The investments that yield most reliable returns are going to be clustered in industries which Russia is already competitive in for many cases. The trouble then is that these industries are responsible for distorting the current account and distribution of wealth nationally and hostage to price cycles that, as I’ve laid out in different ways, they cannot control or necessarily do that much to adjust in response to. It gets worse. Russian extractives and industrial manufacturers maintain artificially high levels of employment and suboptimal levels of productivity to curry political favor and due to the frequently competing incentives between political relationships, slapdash regulatory regimes, and tax burdens adjusted as needed for the budget. In order for them to realize their actual potential levels of productivity, competitiveness, and tax receipts for the budget, they’d have to shed jobs. Unemployed people probably like the regime less, and the only way to stave off a related employment-political crisis is therefore to spend bigger and create more ancillary employment from how capital is deployed, particularly for the services sector. Basically, Russian macroeconomic policy has learned the wrong lessons (for the right reasons) from its own past struggles with Soviet budgetary politics and the default of 98’. A stagnant economy reliant on rents — resource-based or administratively-generated via onerous and inconsistent regulation — can only generate adequate non-rent tax receipts and economic activity to truly escape the structural impacts of over-reliance on resource exports denominated in a foreign currency and external demand by spending more and there is no evidence of a hard budget constraint at the national level as of yet. The paradox of thrift applies to the national balance sheet, especially when global demand is suppressed.

Now back to optimization. Mishustin’s gambit is the step that tends to precede big efforts to reform in Russia’s political economy. Before one can undertake an economic program to ‘break out’ of a stagnation trap, it has to be able to administer resources well, avoid extensive corruption, and address the ever-present risk of state and business capture within Russia’s political system because of its excessive centralization of power in the hands of the president or leader. In the same way Gorbachev spent his first year in power fighting to fix investment strategies and save the economy as it was before being able to reform it. Improving the efficiency of the administration of resources should, in theory, make future reform more palatable and successful. In reality, it does the opposite. Any future success that weakens the political settlement underpinning the current system leads to a new set of problems. In Russia’s case, COVID is going to be terrible for SMEs and they’re going to suffer a great deal more than the countries’ largest firms, no matter how badly run they often are.

Mishustin is doing his job. He’s a technocrat and sticking tightly to his brief. But optimization is a first step to underline the real reform process doomed to failure. One might expect a gradual further adjustment period between the oil & gas and non-oil & gas shares of the consolidated budget, but that has to be reflected by a broader turn towards an economy more heavily driven by domestic demand. That entails a whole new set of tradeoffs when it comes to taxation and the political power of different sectors, tradeoffs I’m quite skeptical anyone high up in Moscow wants to make. Sometimes you have to spend money to make money. Mishustin and the budget hawks in Moscow need to realize this reality. The sooner, the better.

Eurosteppin’

The ECB’s run out of ammunition when it comes to moral suasion and promises. The consolidated recovery fund budget for the EU is now in jeopardy — Hungary is set to veto with a looming threat from Poland over stipulations regarding the rule of law. Europe is in a terrible spot for a reflation trade, and Russia’s exposed to the fallout.

The US is now in the midst of a new infection surge of mammoth proportions thanks to its sainted leaders in the White House and congressional leadership in both parties playing football with the lives of the public:

To top it off, China’s economic recovery may be “broader” but the relative gap between the recovery in industrial output and consumer demand actually continues to grow:

Russia’s long bet on external demand is going to be a massive flop if global coordination doesn’t emerge quickly and decisively.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).