Bull in a China Shop

The swift evolution of the Biden administration’s approach to China reinforces the case that Biden’s approach to foreign policy may differ in style and openness to multilateralism, but is for the most part a continuation of what the Trump administration was doing. With the exception of Israel — increasingly polarized within the Democratic Party as well — and Yemen — a useful symbol to appear to ‘resist’ Trump — US policy is on the same course as before and, what’s more, with the buy-in of the vast majority of both sides of the aisle. Washington actually didn’t have much of a serious problem with Trump’s foreign policy in terms of its aims and operating assumptions about power or interests, but rather its unpredictability and impotence at leveraging alliances and existing relationships to achieve ends. The dustup between Secretary of State Tony Blinken, National Security Advisor Jake Sullivan, and their Chinese counterparts at a brief summit in Alaska predictably aroused panic, interest, and intrigue from the full spectrum left to right in foreign circles:

What was more interesting than the standoff, clearly intended for domestic political consumption as much as an elaboration of a clear ‘position’ on China, was the announcement thereafter from the Japanese government of its intention to cooperate with the US to respond in the event that Taiwan was attacked by the mainland. Blinken pretty obviously choreographed the hit to then signal that we’re working more closely with allies to push back, now further strengthened with coordinated human rights sanctions on China negotiated between the US, Canada, and EU. There’s no end to the tariff war in sight, either. Useful graphics from PIIE on just how much higher tariff rates are between the US and China vs. the rest of the world:

The Biden administration won’t be lifting those tariffs until they get something in return. Since I doubt they will, save perhaps on climate issues, the default is to take the Trump administration’s approach on trade. Punish for leverage. The difference is in Biden’s ability to negotiate with and manage relationships with other states that could affect the balance over time. We’re locked into confrontation, and I don’t count myself among those panicked about a potential Cold War. Most of these fears are rather naively founded on the assumption that China doesn’t get a vote in the matter and that there is no way to sincerely address issues like the loss of manufacturing jobs without a significant macroeconomic and geopolitical adjustment on the part of the United States. Every time these adjustments occur, there’s hell to pay domestically. One only has to look at what Nixon and Ford attempted (and failed) to sustain as Carter ripped up the playbook and pivoted the US to commit itself to the use of military force in the Gulf to ensure energy security while the Soviets blew their goodwill in the Middle East by invading Afghanistan. In the same way hawkish neoconservative Democrats and their Republican partners in the Senate killed Nixon’s detente and boxed in Carter, the hawkish consensus on the Hill today concerning Iran and China as well as that of Biden’s own staff picks, many of them products of the party organs that the Clintons have historically dominated since the 90s, have boxed him in as well. Add that ceding any ground on trade and China would be seen as a betrayal of American labor and you have a rather odd constellation of lobbies and forces with vested political interests maintaining the status quo that Trump launched, but with a much greater degree of competence and willingness to negotiate.

At the same time Biden is locked into the same glide path on China, his revealed preference not to reenter the Iran Deal has finally begun to set in for the handmaidens to power in Washington, generally the last to acknowledge the elephant in the room. In a piece for the The Washington Post at the end of last week, Ishaan Tharoor came right out and said Biden’s window to re-enter the deal is closing. We’ve known this since his team signaled they wanted a bigger, better deal during the transition, but here we are. The most visible test for the United States’ ability to coerce Tehran into talking comes from the threat that China will shift from buying Iranian crude cargoes via transfers at sea and different flag designations for tankers and instead just outright buy Iranian crude unencumbered. Beijing’s game of chicken comes just after the Iranian South Oil Company announced it had raised output by 30% at its fields, part of a broader ‘reassurance’ effort that the Iranian oil sector is doing fine. An escalatory spiral with China this does not make, but Biden’s far more willing to put his foot on the gas diplomatically and appears to be happy going hell for leather. Oddly, the biggest problem for the relationship might actually be US stimulus plans.

This afternoon, D.C.’s paper of record reported that the infrastructure bill currently in the works is pegged at a combined $3 trillion with serious expansions of current welfare measures through 2025 (perfect election timing!), universal pre-K, national childcare, policies aimed at increasing women’s participation in the workforce, as well as what you’d expect in the form of big green spending commitments and the big infrastructure push promised as part of the “Build Back Better” branding. Should it pass, then we’d have to adjust the United States’ growth path even further upward. Adam Tooze posed an interesting question on Twitter: how we square the insane over-performance of US equities against international competitors since 2010 with narratives of American decline:

For now, we should expect that trend to continue especially with Europe blowing its recovery spectacularly with the new round of lockdowns and vaccine drama. It’s important to note just how much of the US equities market today is held by foreigners. Note that these figures go back to 2016-2017, but that the trend has most likely continued apace, particularly since the Trump tax cut juiced returns via buybacks:

US deficits are likely to generate greater private sector earnings as consumption goes up with spending measures, which is going to look better if you’re hunting for yield and stability. That means more capital flowing into the US, the potential for a strengthening dollar, and a harder time for some emerging markets to attract capital. But US pulling this off — let’s assume for now that a large spending bill is going to pass, though perhaps not all $3 trillion — is not great news for everyone else necessarily. Russia, Brazil, and Turkey have all hiked key rates to try and head off inflationary pressures. There’s the emerging market angle to consider, though much of that has to do with a synchronized upsurge in commodity prices buoyed by the distribution of the effects of the pandemic on demand and business investment. China’s got plenty to sweat with the shift in US policy given its own supply-side approach and concerns about financial instability.

Chinese equities have been hit hard by China’s pivot to clamp down on financial risks, reducing the flow of credit and liquidity for investment into equities and, more importantly, real estate given that real estate valuations play a huge role in propping up the economy. But the real estate bubble has to be eased for the sake of sustainable growth and levels of leverage in the economy are a systemic risk. The effect of the latest de-risking effort has been deflationary for Chinese equities:

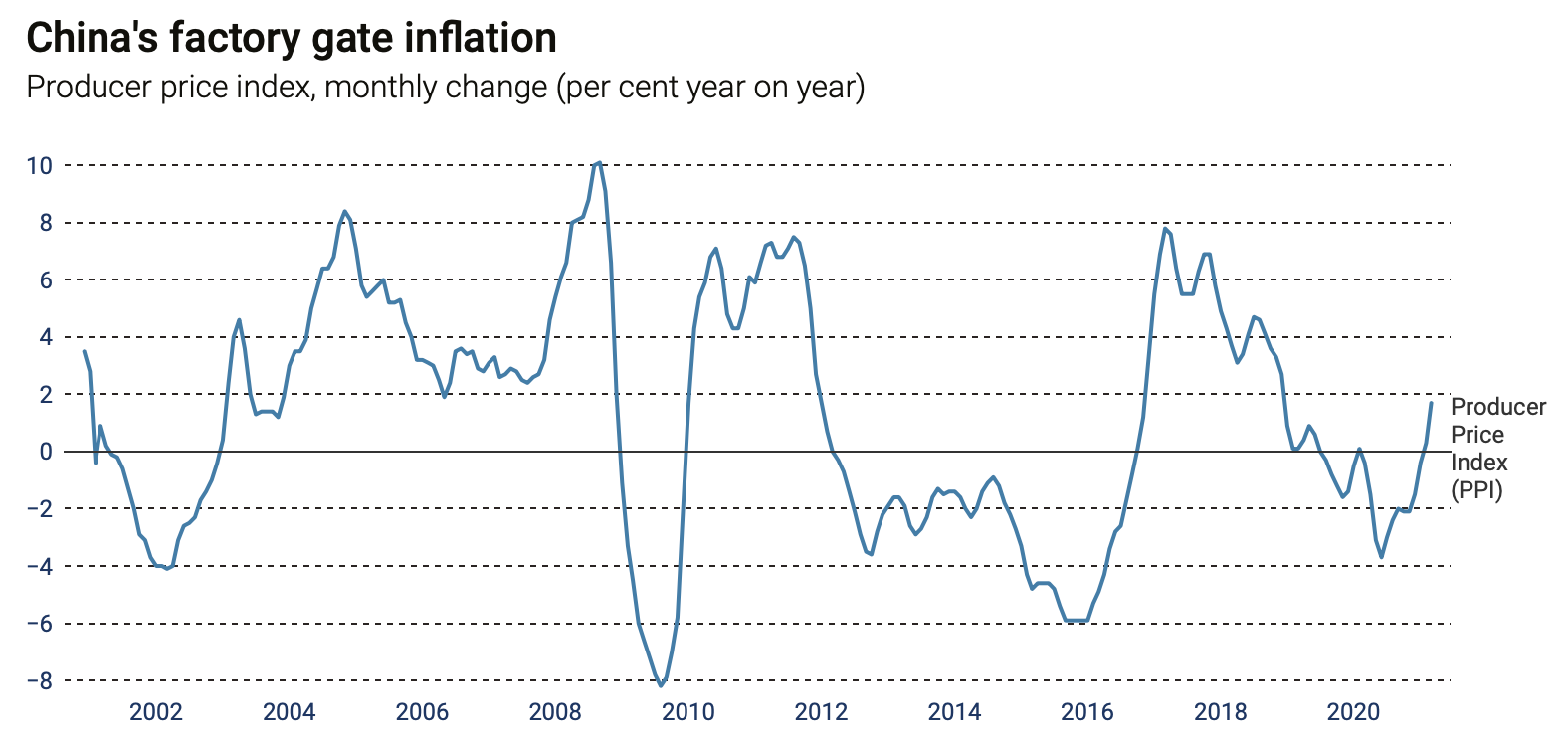

The flood of capital into China last year hoping to realize better returns will shift some in composition and outlook the more that the US deficit spends, pressuring Chinese policymakers to maintain growth as asset values take a bit of a hit. The related risk is the transmission of inflation via US fiscal expansion as the US dollar depreciates, affecting the USD/yuan exchange rate, the large volume of US Treasuries held by Chinese investors/banks, and, once again, asset values because of the $3.2 trillion in USD reserves sitting on the state’s balance sheets. Fluctuations in the USD exchange rate are all the more worrying because of the composition of inflation currently being experienced in China. Producer price inflation is rising while consumer price inflation isn’t lifting up:

Producer price inflation is of considerable concern if it sticks for longer since it affects export earnings, and therefore exchange rate management and asset values in the Chinese economy. CPI remains low, but could potentially benefit from spillover from the US depending on what activity US deficit spending helps in China domestically. But if CPI rises alongside PPI, well, then inflation risks are likelier to prompt tighter monetary policy, which means slowing down growth more in a manner that the US doesn't seem likely to follow since the Federal Reserve is committed to hold down rates through 2024-2025 until what it deems full or close(r) to full employment is achieved. The growing complexity of the interaction between the financial sector and China’s real economy, therefore, poses a massive pressure point for future economic talks since Beijing may well see rising US deficit spending as irresponsible and displacing inflation and economic adjustment pressures onto China and other economies. The fun’s just beginning if Biden’s serious about US manufacturing exports, though I suspect that’s more about packaging and strengthening wages and collective bargaining power than considerably improving the sector’s competitiveness, though a weaker dollar from higher spending levels could help around the margins.

So far, Biden’s off to an impressive start in beating China at their own game: growth and structural economic power. But the degree to which these developments pose future instability risks and could be derailed by the more militaristic personnel and aspects of Biden’s foreign policy can’t be ignored. His sales pitch on the campaign trail was to act as a caretaker president, someone to clean up the mess Trump made. It just so happens that he’s stuck being a caretaker for a painful economic and geopolitical adjustment process that always complicates domestic politics come midterms and presidential elections. Here’s hoping the current run lasts. The eyes of the world now turn to Joe Manchin, Krysten Sinema, and the vagaries of filibuster reform.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).