Good News for People Who Like Bad News

Interesting Tidbits

It’s too soon to tell how healthy Russia Inc.’s balance sheets are, it seems. September monitoring from the CBR for January-August showed that corporate borrowing on an annualized basis was up 9.4% against a 6.4% rise a year ago, and up 13% for SMEs against a 2.9% decrease from last year. Though it seems that concentrated lending from one bank to firms in the extractive sector accounts for the sudden uptick in borrowing seen in August, there is a steady worsening of the quality of credit being held, which should worry policymakers.

Vice Minister Victoria Abramchenko, at the behest of the Fishing Fleet Shipowners Association (ASRF), is directing Rosssel’xoznadzor to hurry up renewing the list of qualified firms for sales to the Chinese market to be provided to their Chinese counterparts at upcoming negotiations. Some estimate expanded market access would yield an additional $120 million annually, and crucially provide a small but important lifeline to businesses in the Far East (which certainly wouldn’t hurt in Khabarovsk, at least). It’d also support Prime Minister Mishustin’s proposal to create at least 450,000 jobs in the RFE through 2035.

Gazpromneft and Tatneft look set to receive tax breaks worth up to 36 billion rubles ($451.4 million) each for 2021-2023 to reduce the relative increase of their tax burden from MinFin’s reforms. The tax relief is targeted at Tatneft’s Romashkinsky field, whereas Gazpromneft is getting a break for its Novoportovskiy field. The relief is designed to offer 1 billion rubles ($12.5 million) every month, clearly aimed at propping up service contractors during an extended period of oil price uncertainty.

President Putin has let governors know that another stringent lockdown isn’t on the table. Seems instead that in the event of a second wave, herd mentality will hold sway.

Share of organizations carrying out technological innovations from their sectoral totals:

All: 19.8% Extractives: 9% Refining (and value-added production): 27.9% Power generation: 7.7% Water supply: 3.7% Agriculture: 5.4% Construction: 9.5%

Russia’s got a problem: its economy lacks complexity. It’s notable that value-added refining leads the way for technological innovation because it’s a somewhat deceptive figure. LNG production is technically a refining process and the investments into natural gas refining for end products demand by Sibur, for example, would skew the numbers in practice. That doesn’t mean there is zero innovation taking place for value-added production, but rather that building more complex refineries isn’t going to yield enough value-add to help Russia return to growth so long as it’s concentrated in pockets of the energy sector that are going to lose from first declining demand growth, and then declining demand while other countries host much more complex refining bases due to the prior waves of investment into the downstream outside of Europe.

Escalation in Nagorno-Karabakh

I won’t pretend to have anything insightful to say about facts on the ground. The most recent post by Armenian minister of defense Shuman Stepanyan suggests that total mobilization wasn’t a bluff. Things are going to get worse and the reports of Syrian rebel fighters being recruited by Turkish security companies to move to police the Azeri border does not augur well for a peaceful deescalation. The only thing I can add as meaningful context is the political economy of Baku’s decision to kick this off now. Next year’s budget assumes an oil price of $35 a barrel and that’s not great news. As Alex Nice noted back in April, Baku refused to adjust the manat exchange rate to reflect the collapse of oil prices:

It’s still hanging at 1.7 manat to the USD, which can only mean that the Central Bank is scrambling. SOFAZ has beaten expectations and maintained a valuation of about $43 billion, but it looks like the appreciation of gold - about 13% of its holdings - and the Euro - about 20% - have probably done the heavy lifting while one imagines that it’s used money market operations to help the manat. The exchange peg simultaneously maintains household spending, and therefore support for the regime, even though it undermines non-energy exports. Oil prices are going to be stuck in the doldrums for the foreseeable future. Until vaccines work and are distributed, we can’t talk about returning to normal activity, and there’s little positive news about demand coming back full strength. Jet fuel alone accounted for roughly 8% of global demand - around 8 million barrels per day - before COVID struck, and that’s going to take awhile to come back. Maintaining the peg can be managed with some nifty hedging on the part of SOFAZ and the Central Bank, but not easily and not without growing economic costs.

This is a rather cold and dispassionate way of saying that the current oil market environment provides little reason for Aliyev to back down. It’s not now or never, but the regime’s ability to make use of its military relationship with Israel, import better military equipment etc. will diminish in relative terms over time without another bull oil market run to sustain high prices. That’s been true since 2014, but adjusting to a lower price ceiling is far different than adjusting to the potential death of demand growth. There are many other, likely more salient factors playing out right now, but it’s important to remember that the domestic instability generated by petroleum revenue dependence can foster conflict via boom-bust cycles.

The Triple-shot

There’ll be plenty more to come on the impact of US elections across the globe, but it’s worth flagging that Alfa Bank’s Natalia Orlova has laid out a scenario where a Biden victory come November will send the ruble towards an exchange rate of 100 rubles to the Euro. Her scenario basically assumes that we could expect US-European relations to normalize after, which one would expect to increase sanctions pressure post-Navalny and help the Euro strengthen. The trouble with the takeaway is that a stronger Euro has been evidence of deflation across the Eurozone, not strength. With a hat tip to Robin Brooks from the IIF (note that this would tend to understate misalignment from fair value):

In effect, the Euro in 2020 is significantly overvalued at the same time that the European Central Bank keeps falling short of inflation expectations and August saw deflation across a majority of Eurozone economies. Biden winning does nothing for the structural problem of global economic imbalances, nor does it even guarantee that Democrats control the senate or agree on aggressive stimulus. What is interesting is that the appreciation of the Euro has improved Rosneft’s profits ever since it switched to Euro-denominated contracts last November, and also boosted Russia’s reserve valuations. Rising profits, however, are linked to a likely acceleration of declining demand in Europe.

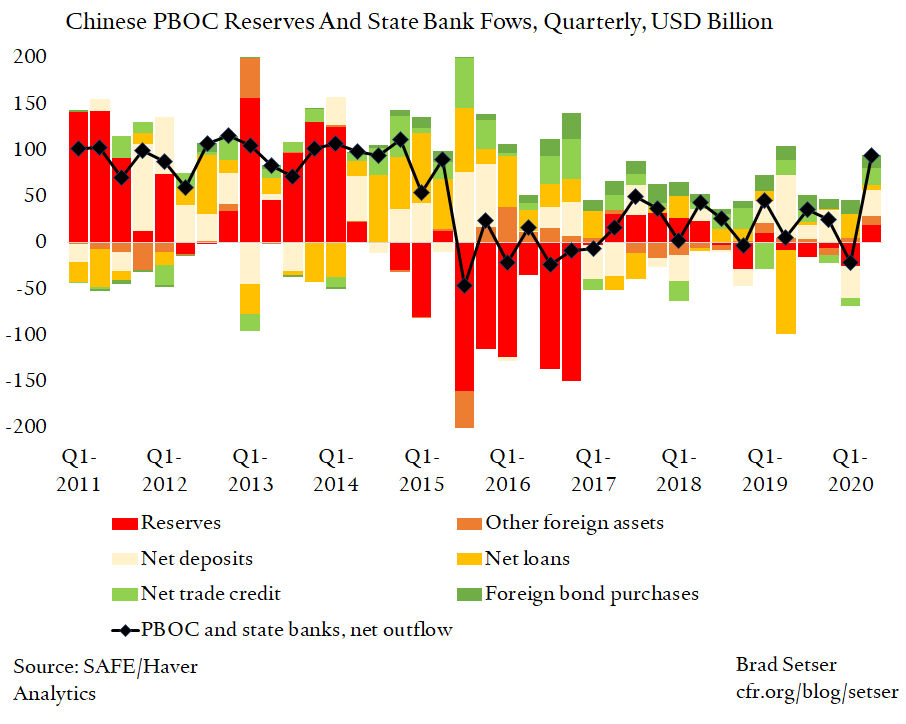

Though oil had made up lost ground in the EU since 2008, it never reached the same demand levels, thanks in part to a decade of austerity. The urge to spend bigly now is going to funneled towards green ventures which, however flawed, will hurt long-run oil and gas demand. The perverse truth for Russia’s energy sector is that the lower the ruble falls, the better off its profits will be in relative terms. But the story gets more complicated with China. CFR’s Brad Setser points to the surge in net outflow for Q2 in China:

China’s begun running a sizable current account surplus again, with the US absorbing much of that from its own stimulus plans. But a Biden victory doesn’t necessarily matter for stimulus plans till January. A rise in the current account surplus via exports puts the RMB under considerable appreciation pressure, and the net outflows in 2020 are reminiscent of past attempts by the People’s Bank of China to avoid appreciation in order to sustain exports and, therefore, employment in exporting sectors. Orlova’s scenario called for the ruble to settle at 70-75 to the USD and more optimistic hopes that Brent crude comes to trade closer to $50 a barrel. That’s missing the problem. The Euro is too strong - good for Russian firms earning in Euros, bad for Eurozone growth - the USD is being held down by the Federal Reserve doing its damnedest to get Congress to pass more stimulus - and the RMB is tipping towards being undervalued if its export levels sustain. The ruble would more likely strengthen if the RMB strengthens since that would support yet more oil demand among Chinese consumers, and by extension help push prices up. But overall, you get a situation where everything that could maximally support oil prices isn’t aligning structurally and positive gains for specific Russian companies and its reserves herald bad news for growth and incomes.

Liked what you read? Want to see how it develops? Subscribe! You know you want to. And if you want to, but are a student or professor navigating the insanity of COVID-19, DM me at @ntrickett16 or else email me at nbtrickett@gmail.com and I’ll forward you a link for an 80% discount. Just want the free plan? All good! Please share with your friends and colleagues if you think it’s interesting.