Top of the Pops

This morning, Brent crude prices were reacting positively to news that OPEC+ his expected to roll over the current supply cuts tomorrow through May-June after an OPEC+ panel noted that rising infection rates posed greater uncertainty for demand in 2Q and H2 this year and cut the demand outlook for 2021 by 300,000 barrels:

Russia’s angling for wiggle room to increase its own output levels, something sorely needed for midstream profits since Transneft recorded a 26% decline in net profits last year from output cuts and COVID-19. The real lesson here is that it’s not just China that can’t prop up oil anymore, but China and the US experiencing stronger growth. We might see a different geography of shifts in marginal demand driving price changes post-COVID, though it’s still a little early to be certain. Much was made of the “$400 billion” 25-year strategic partnership agreement signed between Iran and China since it could have a long-run impact on oil output and supply/demand balances, yet China’s own foreign ministry stressed that no actual deals were signed. Mehr News has pushed out a piece claiming that Iran is now ready to sign a similar long-term agreement with Russia to “neutralize” the impact of sanctions. Given that the China agreement has no teeth, this is clearly PR fluff. Russian firms have avoided investments in Iran since Trump came into office in 2017 fearing sanctions reprisals (which were reimposed on Iran in the end) and also struggled to negotiate terms with Tehran. All of the reporting from 2016-2017 suggested massive interest from Lukoil and Rosneft, but no substantive progress. So that bet is off, it would seem, so long as US sanctions remain in place and isn’t factoring into future price considerations for now. Price stability is also in the government’s interest as it moves to introduce new support measures to stabilize wholesale fuel prices now rising higher than retail prices in many regions, preempting further price inflation. I’d expect Russia to get minor output concessions but not push for too much as the producers’ bloc is probably stuck holding the cuts in place till August, but may marginally up output before during the summer.

What’s going on?

As if the current food and production price inflation wave wasn’t enough for milk producers, they’re going to be hit with new ecological regulations as of Jan. 1, 2022 that they warn could raise the production price of milk 10-15%. Company lobbies love to exaggerate, so always consider the source, but the contention is that mandating companies recycle all packaging will raise costs, as will the doubling of ‘ecotaxes’ on those producers who can’t do so. It’s logical to raise the regulatory requirement and maintain some sort of mechanism to punish and reward firms accordingly, however the current proposal seems destined to spur more consolidation among producers while raising costs at a time when incomes can’t keep pace. At present, producers are spending 19.2 billion rubles ($254.2 million) to cover ecological expenses while receiving 9.4 billion rubles ($124.46 million) in subsidies. It seems an easier way to manage the ‘punishment’ would be to withdraw subsidy support for producers who can’t meet the requirements, but this then ends up harming demand for goods and services from other firms I suspect. Either way, the expected additional 5-6% retail price increase for milk after a year in which the price increase will almost certainly outstrip topline inflation significantly is a big problem for households. The RUIE is lobbying to reduce the recycling requirement to 35% and lighten the transition, but it’s unclear how successful they’ll be. The real lesson is that the Russian economy is now paying for the frequently delayed process of implementing regulatory changes to better align/harmonize practices with the EU/West, or in this case in response to local political protests.

A survey lead by BCG along with The Network and hh.ru shows that most Russians want to retain considerable flexibility to work from home multiple days a week. This obviously can’t apply to site-specific work, such as brick & mortar retail jobs, extractive industries, or manufacturing, but the shift in attitudes from the experience of the pandemic could put a lot more pressure on Russia’s housing market as employers adapt. Red is Russia, blue the world average response:

Title: Desired # of working days out of the office, % respondents

While the Central Bank is starting to pull back the crisis mortgage subsidy program, there’s a new one in the works that’ll matter soon enough: a “green mortgage” scheme to spur on the construction of green homes. Given the policy-induced shortfall from the spurt of buying, the only way to spur private-sector demand separate from the federally/regionally funded housing program will be more supply side measures barring any additional income support or significantly redistributive policies. But the welfare system is miserly and designed to force anyone living in a city to work since unskilled jobs pay higher than unemployment benefits. That’s why the change in attitudes about working from home is so important. Even if just 10-20% of office workers transition to working from home most of the time, that’s realistically a huge bump up in space needs for those living in cities (unless they already have the best digs), or else pressure to move further away from city centers. This then creates knock on local housing price pressures, affects transit systems, and so on. The question is whether or not people will be earning enough to do so. So far, the recovery suggests most face significant financial constraints.

MinEkonomiki has rewritten the National Goals for small and medium-sized businesses to aim for the much simpler metric of increasing SME employment to 25 million people out of the national workforce officially in the range of 72ish million, not including the gaps that likely exist tracking illegal/semi-legal migrant labor, by 2030. The SME % share of GDP target was scrapped entirely — originally the intent was to have SMEs account for 32.5% of GDP, up from the current 20%. So what does this tell us about Russia’s economic policy? They have no intention of expanding SMEs’ share of the economy and, crucially, as long as the workforce is declining in size or else stagnant, the increase in employment target is likely viewed as a ‘shock absorber.’ As efficiency gains at SOEs and larger industries from greater levels of automation and the Internet of Things shift labor needs as will the effects of carbon policies, presumably the hope is that SMEs can absorb the slack on the labor market. But not everyone wants to buss tables or work in retail, which is where the net job creation since 2015-2016 has been by and large alongside the growth of the gig economy and self-employment. The main stimulus approach is to provide 800 billion rubles ($10.6 billion) in subsidized credit to businesses every year, but demand is likely to outstrip that figure. The other problem with the subsidy credit approach is that the real rates across the economy are affected via the trade surplus and budget balance, which means the continued suppression of domestic aggregate demand, harming the underlying consumer demand for SME goods and services so long as the current orthodoxy holds. They’re basically giving up on material progress and hoping that cheap credit will fill in the gaps.

The governors of St. Petersburg, Murmansk, Archangelsk, Kamchatka, and Sakhalin are calling on the government to form a development plan for a “big” Northern Sea Route linking St. Petersburg and Vladivostok. They claim it’ll speed up delivery of goods between regions and support greater utilization for container trade between ports within the country — cabotage trade for those who like regulatory arcana. Their thinking is simple: rail routes don’t serve most of these Arctic regions very well and there’s inadequate support for sea freight via the NSR. Murmansk seems to be out front asking that RZhD reintroduce discounted tariffs to send freight via Murmansk, lower the tariff rates for icebreaker escorts, allow ships to travel without an escort when they’re in ice-free areas, and to use regional funds to invest into expanding and modernizing port infrastructure to support the new route. My confusion comes from what they’re going to use to make the route viable financially and to meet the volume targets for the NSR. Shipping fish from the Far East to St. Petersburg is one thing — I highly doubt Murmansk will be importing too much of it given its nearer to other fishing basins — but the main driver for new output will be crude oil, ostensibly from Vostok Oil. Rosatom is obviously banking on more consumer goods trade via the route, and leapt to exploit the Suez blockage to sell the NSR. The route’s 30% shorter. But so long as it lacks auxiliary markets to absorb cargoes when they’re re-routed or orders canceled, it’s hard to imagine it’s going to displace too much traffic from Suez, whose routes traces a much broader range of large markets with more consumers and capacity.

COVID Status Report

8,275 new cases were recorded along with 408 deaths. Based on the week-on-week % decline rate lately, you’d think that Russia’s in for good news regarding the pandemic:

You might be wrong. Fears of a 3rd wave of infections seem to be mounting as deputy health minister Tatiana Semenova has warned that it’s a real possibility. Gaps in the vaccination campaign remain the problem and the 3rd wave now being seen in France and other parts of Europe seems to have spooked some officials trying to get ahead of any potential resurgence in the case load and the ongoing risks of mutation. Clearly the excess mortality data shows things are still worse than these figures imply, even with an assumed case decline rate of that magnitude, and we’re still wondering whether or not the sheer number of infected people has given rise to greater immunity locally in many contexts. The observation from Europe is that cases picked up once things warmed up, and Russia warms up later than Western Europe. So much for the strength of Russia’s COVID response.

Arrested Development

The World Bank’s release on debt data concerning developing countries and their creditors revealed that as of the end of 2019, Russia was the world’s 5th largest sovereign lender to developing countries. Russian loans were worth a combined $22.9 billion, way behind China ($149.1 billion) and Japan ($107.1 billion) and closer to Germany ($28.3 billion) and France ($27.3 billion). On a ranking basis, 5th is impressive. It just beats out Saudi Arabia and the US came in at #10, though that’s more a function of the US relying on private sector lending and fact that other sovereigns lending in USD are effectively linking their own efforts to the US financial system. What struck me seeing that figure was how much lower it was than I’d have expected given Russia’s large trade surplus and the shift after Putin’s Munich speech in 2007 to more aggressively embrace BRICS as well as try to diversify economic relationships in Africa and, more broadly, among developing economies. The figure also reveals just how miserly the Russian state has been even during boom years as well as the large outflow of private capital corresponding to that trade surplus that more often than not ends up circulating mostly through offshore banks, speculative investments, or assets meant to store value rather than supporting real economy activity in the CIS or west. Think Germany’s trade surplus recycled within the EU into real estate investments in Spain and Greece, for instance. Since the state accrues so many reserves, I was surprised that Russia only lent about $4-5 billion more as a sovereign than Saudi Arabia.

Pulling up the macro overview from the World Bank statistical report that inspired the coverage in RBK — the country-level lending data is from MinFin and other related sources and a lot harder track down — we can see/infer some interesting tidbits:

Debt servicing costs are amply covered by export earnings and have trended downwards as a % of exports, even with current account compression from lower oil prices. Reserves to external debt stocks, private and public, rose significantly from 2016 onwards after the 2014 shock. Bondholders held a significantly rising share of private credit, which corresponds to sanctions risks for foreign commercial lending into Russia, but I think also reflects a broader expansion of the domestic bond market driven most strongly last year by OFZ issuances. Unguaranteed private sector debt (read: the government does not guarantee these loans) has been stable at around 46-48% of the net debt stocks since Crimea. External debt to the national income trended downwards after the initial banking crisis and recession in 2015-2016, and similarly reflects both austerity and the growing politicization of borrowing i.e. subsidy programs, formal or informal guarantees, SOE-led borrowing that’s legally classified as private sector in Russia, and other accounting tricks. There’s also a broader change observable among emerging markets after the Federal Reserve induced 'taper tantrum’ of 2013 and the appreciation of the USD in 2014-2015 alongside the European Central Bank’s introduction of negative interest rates:

Short-term debt fell off trend with public guarantees broadly accounting for a slightly higher share of borrowing post 2015-2016. Given Russia’s considerable currency reserves and expanded geopolitical interests, you’d think they’d have tried to up their lending game, particularly since publicly-guaranteed debt issuance took a larger share of EM borrowing post-Crimea. But they would have inevitably run into the problem that if a developing country wants to hedge or manage exchange rate risks, they likely want to use US dollars or Euros rather than rubles. The fear of USD dependency linked to sanctions risks deters lending after Crimea. But even before, it wasn’t like Russia was playing a particularly constructive financial role using its reserve accumulation to back lending at scale that could have significantly aided development across Eurasia and further afield. Some of this probably stems from the composition of debt exposure. Though Russia had, in theory, enough foreign currency reserves in hand during the worst of the shock in 2014 to weather the storm, Russian corporates affected directly by sanctions or by reputational sanctions risks would need to pay off at least $100 billion in foreign-denominated external debts for 2015 despite benefiting from the ruble devaluation driving down the nominal value of foreign-denominated debts owed in many cases. But it should be little surprise that a sovereign that mismanages development domestically is likelier to be more reticent to lend to developing countries because of the large amount of learning involved: sovereign lenders in developing markets have to manage local risks, default risks, business cycles — commodity booms tend to foster more reckless lending that ends in tears — and so on.

Consider the volume of sovereign lending China does vs. Russia per the 2019 data and their comparative road construction in the 2000s. It may seem a bit off topic, but I think it’s useful since these projects are broadly guaranteed by state financing or guarantees to the private financiers underwriting the projects and a core competency for development lending is properly assessing costs and managing expenses. One of the bizarrely under-appreciated aspects of the boom years Putin enjoyed during his first two terms is that road construction actually fell on his watch despite rising oil prices and state revenues, and much of the statistical increases registered were at least partially accounted for by the legal registration of roads that had been built in the Soviet-period but lacked legal recognition because of the country’s institutional chaos post-collapse:

Russian stats show that between 2000 and 2015, total road network distance covered rose from 535,000 km to 1,045,000 km, which based on the construction data above for roads with a hard surface is clearly mostly just claiming Soviet roads as ‘new’ roads and the inclusion of local roads and streets into the accounting post-financial crisis. If one corrects the accounting for this, the actual number in 2015 was 525,000 km, a net decline since 2000. In other words, under Putin, the rate of road development has been 1/7th or 1/8th what it was in the Russian Soviet Federative Socialist Republic. This is a catastrophic failure, even if you note the higher quality of more recent builds. Of the largest road construction projects since 2000, only one was longer than 1,000 km. Yet in China over that time period, the road network exploded in size as the country’s own version of demand suppression and political economy of its trade surplus was recycled into investment-led growth that, admittedly, became less and less effective over time:

By 2002-2003, China overtakes Russia for construction of higher-quality roads and Russia loses more ground even once the oil price bull market kicks in around 2003. I’d suggest that the domestic institutional experiences managing construction of basic infrastructure influence the manner in which sovereigns consider lending abroad, particularly since sovereign loans to lots of emerging markets are part of a larger commercial arrangement or arrangements concerning valuable projects. There are, of course, also explicitly political reasons for these loans. But since Russia’s not particularly good at developing itself, it’s not likely to be a good partner developing other states. Instead, you see Russian sovereign lending almost as a form of subsidy for strategic sectors relying on export earnings to manage budget costs — defense contracts for weapons systems or parts are often underwritten using guaranteed state financing as are nuclear power projects. When it comes to roads, they’re rent-generators like any other public contract. And while that may hold true at the regional level in China, the over-investment in the economy into infrastructure has generated lots of institutional knowledge that can translate into funding such projects abroad, where Japan similarly has turned its export surplus, domestic development experience, and glut of USD earnings into a basis for development finance initiatives that target quality and standard-setting.

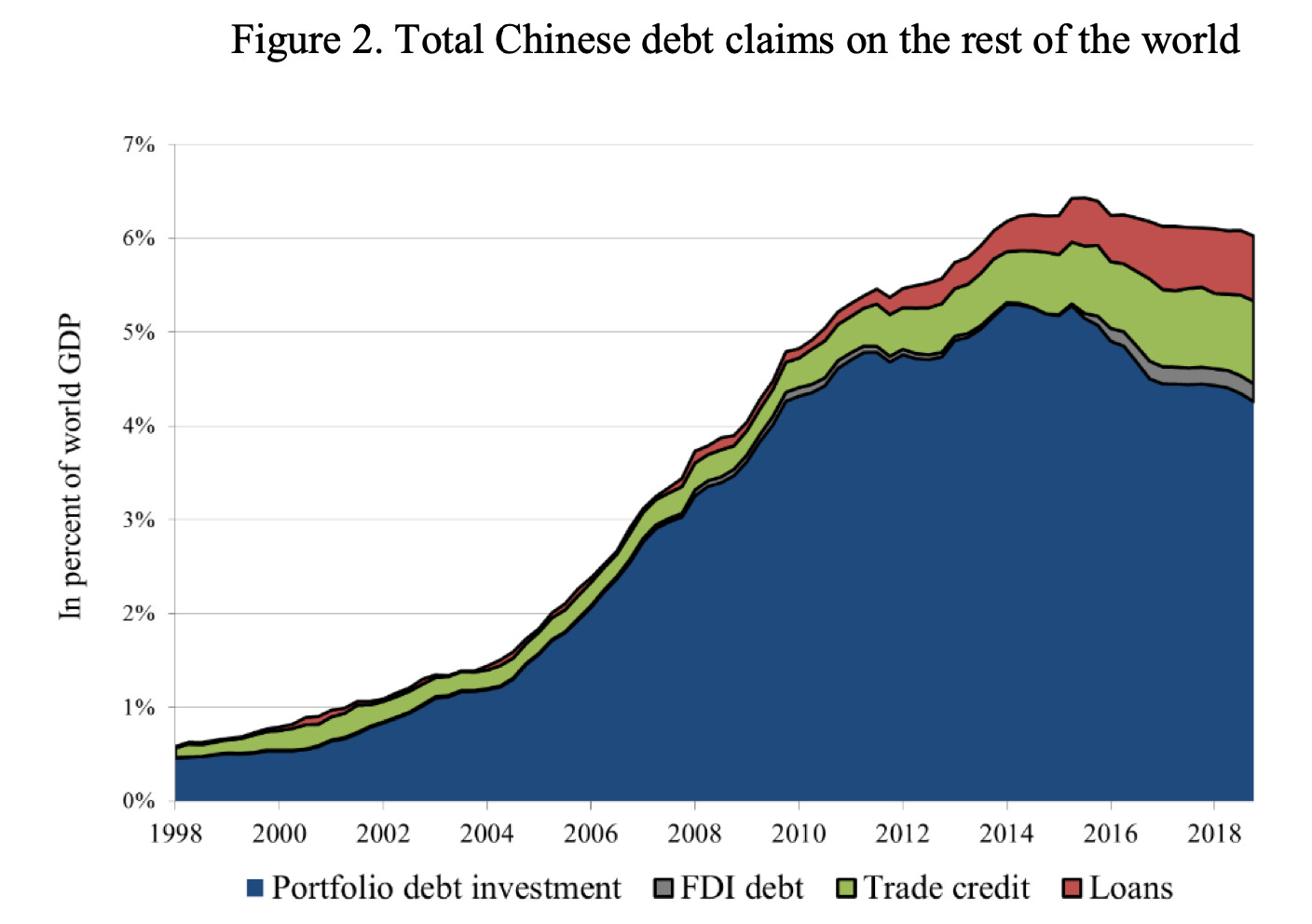

Cobbling these facts together, my takeaway is simple: Russia’s domestic institutional failings on the development front hamstrung its ability to mobilize its export surplus and reserves into an effective vehicle to finance development and (re)integration in Eurasia and elsewhere though it may well have benefited handsomely from doing so. When you take this fact and then add in the reflexive fear of the US dollar and you seriously limit your ability to play that role. China’s a massive lender globally post-global financial crisis, and much of that growth has been led by Chinese banks extending dollar-denominated credit, strengthening the financial role of the USD (though they’re trying to change this now):

Russia is not Iran, and it’s not likely to ever be sanctioned like Iran. It can use dollars and Euros (relatively) freely by comparison. Maybe instead of focusing on trade credits it can leverage those reserves to prop up diversification across the EAEU, for instance, especially since goods could more easily be traded in national currencies. I doubt that’s of much interest for now, though.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).