Quick Hits

Though symbolic and toothless for now, the European Parliament is calling to ban Belarus from SWIFT in response to the forced grounding of the Ryanair flight carrying Roman Protasevich. Safe to say that whatever ‘goodwill’ Minsk — and Moscow — once had with Europe has largely faded, killing future chances of any significant rapprochement regardless of US administration and tack on European defense so long as the two regimes are in power. That’s heated rhetoric calling for Iran-level sanctions…

The government has decided to mobilize the Fund for the Defense of Debtors’ Rights and expand its remit from helping consumers who’ve been swindled in new builds to handing out unsold apartments in problematic buildings the Fund’s been dealing with to families in need of housing. It should speed up helping people find homes, but one can only imagine the red tape and legal proceedings to follow.

Most Russians feel they need 74,900 rubles ($1,044.86) a month to feel financially independent, with that figure rising to 104,000 rubles ($1,450.80) in Moscow. Needless to say wages are far off from those figures.

The Duma’s passed a bill codifying a potential prison sentence of up to 5 years for financing “undesirable” organizations. There’s now really no space to politically organize and operate outside of the “system” anymore so long as they can apply these labels whenever convenient in order to disrupt, discredit, or else punish activity.

New cases are again higher at 11,669 for the last day vs. 383 recorded deaths. Needless to say the trend looks more solid since Moscow maintained higher numbers and, if that continues, the Operational Staff will no longer be hiding the underlying state of the pandemic as much.

Saving Democracy One Mistake At A Time

Biden’s appearance at the G-7 summit in Cornwall amid what is clearly a chaotic, haphazard, and shambolically managed infrastructure bill negotiation process and word that the US forces are ‘halfway’ through withdrawing from Afghanistan merits a bit of thinking about the state of US politics and policy. Whereas 2020 was a year in which, aside from the monumental passage of the CARES Act, the absence of any sort of overriding leadership or sense of agency in Washington defined the affective valence of geopolitics, 2021 has seen Biden stumble into the spotlight after the last stimulus bill, the relative success of the US vaccination campaign since January, and a slew of international efforts restoring some semblance of movement. American power in its fiscal form, at least, has proven more resilient than many expected. But that doesn’t mean enough’s been done. To a degree significantly more salient than probably at any point since the 2014-2015 oil and sanctions shock, economic policy decisions taken in Washington are going to shape a huge part of the economic context for Eurasia in the years ahead. Now it falls to Biden and the Democrats on the Hill and across statehouses to prove they can deliver more.

Let’s start with Infrastructure Month(s). West Virginia senator Joe Manchin has become the de facto face of opposition to the repeal of the filibuster and refusal to pass a huge infrastructure bill through budget reconciliation without a wide array of ultimately unnecessary pay-fors. Inflation hawks and those convinced that the current economic climate is somehow the same as the 1970s — Larry Summers is particularly craven on this score — find their allies among the most ardent institutionalists in the Senate in a protean deflationary bloc able to refashion itself as necessary to justify not spending. There’s a wholly legitimate concern about killing the filibuster. Even with Biden’s national vote lead against Trump, a mere 40-50,000 votes could have shifted the outcome and there’s no guarantee that any ‘Biden boom’ is going to deliver bigger majorities in the House or Senate for next year’s midterms. After all, Democrats managed to lose House seats and only scratch out a tie in the Senate in the middle of an historically bad pandemic taking thousands of American lives daily before the election. For context, West Virginia lags the US national average from the American Society of Civil Engineers (ASCE) for every type of infrastructure receiving straight Ds on its report card. US News ranks it works nationally, along with coming in at 45th for education, 47th for health care, and yet 18th for opportunity. State governor Jim Justice, literally the wealthiest individual in the state, has opted to cut unemployment payments as of June 19. He just so happens to own a resort he was hoping to staff with cheaper labor. Manchin’s a small d “blue dog” democratic senator who eked out a 2018 re-election by 3.3% in a state where roughly 68% of the voters went for Trump in 2016 and 2020. His Washington Post op-ed clearly stating he wouldn’t vote to weaken or repeal the filibuster was basically a concession that we’d be left with the politics of the possible i.e. the meat grinder display of incompetent negotiating now generally producing half-hearted and inadequate proposals. Still, even smaller bills can have a big impact.

The latest bipartisan offers $579 billion in spending without new taxes while sacrificing significant ambition on climate goals. Honestly, if I were Biden, I’d try to get that passed and then tack back to add more via budget reconciliation without Republicans focusing on eliminating Trump’s tax cuts, adding more IRS enforcement powers, and just backloading more infrastructure and climate spending into another bill. No one’s asking me obviously. He’s clearly too risk averse for that, nor is Biden a profile in political courage on domestic issues. He’s made an art of straddling the center of the party and posing wherever on the political spectrum is necessary on a given issue. The ASCE estimated last year that the US would underinvest in infrastructure by $2 trillion from 2016-2025 without proposing any major expansions on growth or climate grounds — that’s not really their focus as an organization. They’re focused on the quality of existing infrastructure. So we’re talking about a large bump in spending to maintain loads of roads, highways, and bridges that aren’t particularly efficient or climate friendly without new and different types of infrastructure investment. With the cost of borrowing so low, it’s truly absurd that a senator from a state that would benefit immensely from the agglomeration effects of expanded rail access to Washington D.C., Philadelphia, Pittsburgh, and Ohio’s numerous mid-level cities can’t fathom the benefits of going big, but here we are. We’re going to get a bill at some point. We just have no idea if the scale will prove adequate.

The compromise version of the Endless Frontier Act, which became the US Innovation and Competition Act, offers a useful counter-example of fairly successful negotiations — an increased spend of $250 billion over the original $100 billion proposal to throw all that money at a new science directorate. In the bill that passed, that figure is down to $29 billion but $52 billion were earmarked for semiconductor industrial capacity. The reality is that you can’t just hand $100 billion to a new agency focused on innovation and expect it to work. In fact, giving too much money to research arms tends to undermine the quality of the research because institutions have to continually justify the massive spend, encouraging more conservative funding proposals for projects that may not yield as significant a breakthrough. Put simply, you need that money to be spent a bit irresponsibly to really yield maximal results. The larger point is that the US is getting comfortable with industrial policy once more. It just needs to do it “better” and embed it into a larger effort to revitalize the national industrial and infrastructural base. These plans can considerably increase demand for key commodities — bitumen from oil, copper, nickel, gold, steel, aluminum, lithium, and more. When you look around globally, US fiscal policy is the most impactful sovereign-led effort that can change commodity markets. China’s trying to cool its own demand and limit price rises and Europe’s doing its usual thing of free riding off of US stimulus. If US efforts to restore some of its manufacturing base are successful, it’s also going to shift the pricing power of US firms somewhat for key inputs over time. On a smaller note, I’m excited to see that Illinois is now creating a high-speed railway commission that will establish an administrative structure to fast-track planning for a potential route linking St. Louis, Chicago, and a series of small cities in Illinois. These structures matter a great deal. You need to have planners to be able to work up the prospectuses to borrow on bond markets and invest at the state level. Local planning power has been one of the biggest casualties of Tory austerity cuts to council staffing in the UK, for instance. Planning requires planners. Who’d have thought!?

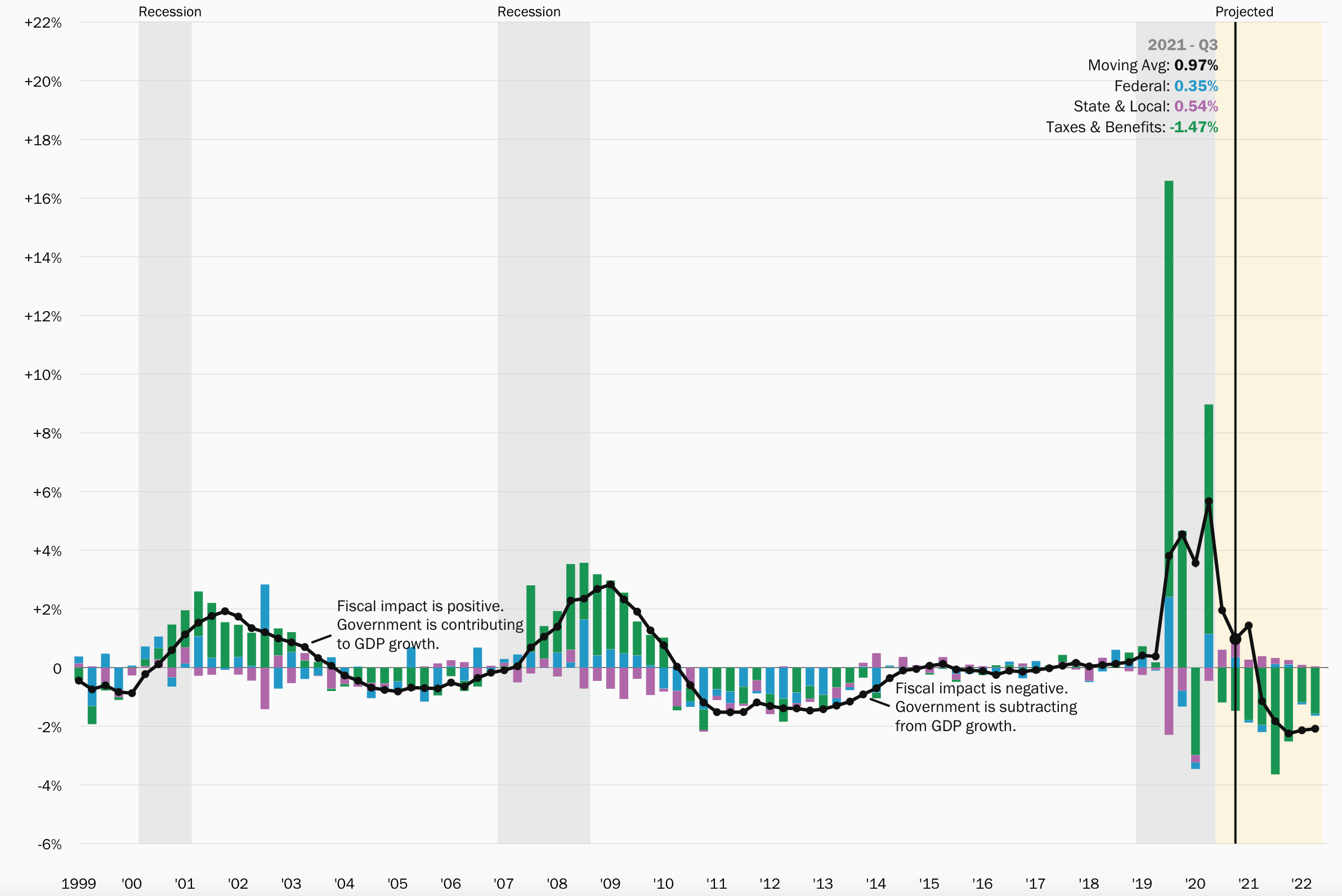

The craziest thing about these interrelated bills and political concerns is that the current fiscal policy effect on GDP growth, as broken down by the Hutchins Center at Brookings, turns negative in 2022-2023 when we desperately need to be sustaining a growth push to lift real wages, maintain strong corporate profits, and fully grasp the narrative Biden himself loves to expound on about a nation meeting the challenge of the moment:

Blue = federal spending on goods/services Purple = state spending Green = taxes/benefits Black = 4Q moving average

All of these factors take place with a Federal Reserve resolutely determined to not raise interest rates until full employment is achieved. These are huge macroeconomic forces colliding with the stories and challenges I cover daily here, and they’re going to shape the next 4-5 years to a considerable degree. They speak to balances of payments, corporate profits, and flows of currency from resource exports across Eurasia — even Russia’s Central Bank has been surprised by the anomalous inflow of capital thanks to rising non-oil & gas commodity prices lately. That doesn’t mean Eurasia’s going to grow. If anything, it’s a threat: resource rent dependence may well deepen due to the new commodity cycle without sustaining more growth, same as has happened with each successive commodity demand shock this century across the region, particularly given higher inflation levels due to commodity prices.

Afghanistan poses a different kind of challenge and change from US policy. Despite having committed to withdrawal, Biden actually hasn’t articulated clearly what the US role is once that withdrawal takes place. As the New York Times just reported, Biden’s national security team led by Jake Sullivan hasn’t yet decided whether or not to provide air support in case the Taliban threaten to overrun Kabul. It’s a crucial detail that hints at Biden backpedaling on the initial framing — the US would only perform “true” counter-terrorism operations when relevant to protect US interests or nationals. A fair bit of the sidebars and talks at the current G-7 summit are almost certainly about the logistics of getting all of our European partners out smoothly, especially given their dependence on America’s military airlift and logistical capacity. There’s now a debate raging about evacuating all the Afghan nationals who helped the US since their lives will be at risk, and taking the Taliban at their word that no harm will come to anyone who worked with the US military would be foolish at the best of times. What’s telling now is that authorities in Kabul are reaching out to Moscow for help.

According to news.ru, Afghan officials are trying to talk through Russia providing military technical assistance with equipment, repairs, and keeping kit in fighting shape after sending a written request to the presidential administration in Moscow. Two weeks ago, Afghanistan’s ambassador in Moscow Said Taib Javad told the Russian press that Kabul is happy to buy Russian military gear and tech if Moscow will sell it. It’s an important turning point for Moscow’s non-strategy in the conflict. They can talk about hosting diplomatic efforts with the Taliban till they’re blue in the face, but they can’t trust the Taliban to take care of potential terrorist threats. On the other hand, they know Ghani’s government will be somewhat reliable on that front. The issue, as always, is how much they can actually trust Afghanistan’s security forces. After the ambassador’s comments, FM Lavrov was clear that Russia’s prepared for any potential military escalation in the county. Early May saw Moscow and Dushanbe agree to launch an integrated air defense system, which goes to show that preparations are well underway to keep a close eye on the conflict and resources available. This is far more a matter of wait and see than the impacts of US economic policy, but nonetheless it appears that Russia has no choice but to increase its involvement, especially if the US decides against providing air support. One possible iteration right now is that Turkey would leave troops in Kabul to secure the airport in exchange for US intelligence support, but nothing concrete has been stated officially. There’s no chance the US is getting a base in Uzbekistan or Tajikistan so we can write that angle off for now. There are also regional economic considerations at play given the current macroeconomic environment of higher inflation. Pakistan was able to concessions from the IMF to delay unpopular reforms because it’s helping the US withdraw from Afghanistan, another classic case of the securitization of the IMF for US policy ends. Food price inflation in Afghanistan was estimated at 10% for 2020, and any disruptions to supplies this year due to security incidents are bound to worsen the globally observed price increase for basic goods. There’s a long list of things that can go wrong and things Russia may have to do to avoid a completely unmanageable status quo while the US Department of Defense turns its focus almost entirely onto China. Russia’s no longer seen as a serious problem for US foreign policy, at least in military terms, and frankly that’s the correct assessment. Interests matter. There is nothing the US needs right now that Russia can block, especially with its own economy increasingly in disarray.

Biden’s off to a very rock start so far disguised by the goodwill engendered from the stimulus bill and reopening with vaccinations. America’s fiscal state is going to have a far larger impact on the next few years of global politics than it did after the Global Financial Crisis. From this thread on an SCMP piece, Michael Pettis reminds us that China’s the economy stricken with a real estate addiction and over-investment now, not the US:

Even seemingly marginal choices made by Washington policymakers may prove to have significant effects for flows of capital, competitiveness, the marginal pricing power of national corporations, and far more. We’ll know more later in the summer as it comes time to actually vote on some of these spending proposals. For now, the G-7 provides another ‘face’ of American power. Trump’s effect on America’s global standing has been grossly exaggerated. So has the US exit from hegemony (which may well be true, but depends more on how one defines hegemony than a decline in power). Diplomacy, or at least its simulacra, is back in vogue. Here’s hoping the global corporate tax deal isn’t gutted.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).