Top of the Pops

Today’s roundup doesn’t have an analysis column as I had a project deadline come up and a bit of a headache with a leaky boiler. Hopefully you make better use of the time saved than I inevitably will.

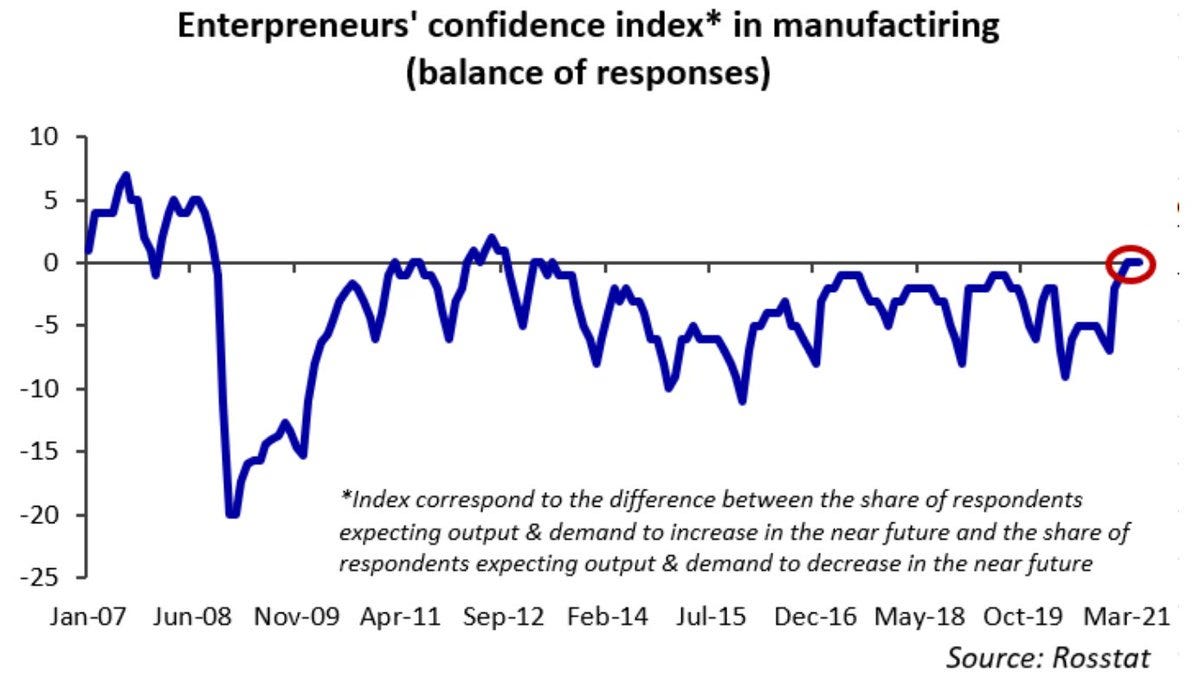

It looks like the current ‘boom’ has nudged business confidence to levels not seen since 2012. But the Rosstat indicators are still in negative territory:

It’s saddening that this is probably the best it’ll get before falling back down. CBR chair Elvira Nabiullina made clear in an interview with Komsomol’skaya Pravda that the 'inflationary spiral’ may accelerate further in the months ahead. Industrial producer price inflation is as high as 35% year-on-year. These costs have to be passed on eventually. Retail costs for goods and services are only up 6% on average. At some point, you can’t hide that by borrowing or betting that inflation will calm down. While Nabiullina is cautioning the market and setting up more rate hikes, the worst bottlenecks causing inflation in the US — the global pacesetter for inflation at the moment — appear to be easing a bit. The worst outliers like lumber are falling in price again. Worth remembering that over half of the inflation registered in the US in May was due to car rentals, used cars, hotels, and airfare alone. Russia’s inflationary pressures are a lot different because of the structure of consumption. Nabiullina’s right to warn that inflation will likely keep accelerating. Commodity prices matter far more in Russia than in the US for changes in relative price levels because those industries are a much larger share of GDP, production, and consumption as well as employment. Early inflation went straight to corporate profits. Now? That dynamic isn’t holding the more pressure companies have to avoid markups for customers.

What’s going on?

The Pension Fund is receiving an additional 500 billion rubles ($6.83 billion) less than what was planned for 2022-2023 because, per MinFin, incomes and insurance premiums are higher than expected. The current 3-year budget assumed that 3.9 trillion rubles ($55.31 billion) would be spent in 2022 followed by 4 trillion rubles ($54.68 billion) in 2023, now to be trimmed by 250 billion rubles ($3.42 billion) each year. For context, 35-40% of the fund comes out of the federal budget with the rest matched via household insurance payments and taxes. This year the fund is receiving 3.3 trillion rubles out of a total of 9.1 trillion shifted into the pension system. What MinFin’s really doing is exploiting an accounting difference from forecasts — there was a 575 billion ruble ($7.86 billion) surplus last year against expectations because the size of the economic shock was smaller than expected since restrictions were never uniformly applied, lots of businesses were forced to stay open, and regime gambled on collective immunity naturally emerging from infections. The argument now goes that the extension of no interest or subsidized loans to businesses did a lot more to lift up real wages and incomes, particularly after Rosstat went back and once again adjusted the data to make the COVID response seem more competent. It’s really a convenient means of pursuing budget consolidation and austerity measures. Cutting back transfers by half a trillion is low-hanging fruit, but also a gamble that inflation won’t ‘eat’ the value of higher incomes and premium contributions assuming they’re right about the data. It’s also backed up by nearly 2 million Russians failing to receive what they were fully owed by non-state pension funds last year because they weren’t aware enough to contest what they got and also excess mortality and the pension reform triggering a record decline in the number of pensioners this last year. These are morbid accounting maneuvers hoping pension ‘education’ can cover the gap. We’ll see.

To give you a sense of the scale of the price and demand uncertainty for the oil market, Castleton Commodities International’s oil price forecast has a range of $35 a barrel to $130 a barrel in the years ahead. In the immediate term, expectations are that the oil market will be tight and see some initial post-COVID growth driven by developed markets. That’s why Russia’s pushing for an output hike with OPEC+ and why Brent crude prices have broken the $75 a barrel barrier in the last day. Confidence in future demand has cemented itself despite the large uncertainties that remain. For instance, European air traffic is still half its pre-pandemic levels and we have every reason to expect regulatory, carbon price interventions, and a new infrastructure push to shift more travel to railways:

China is now drawing on its reserves of crude oil, much of which it bought on the cheap last year, because it now sees the oil price as too high to warrant splurging on imports while Asian demand more broadly struggles to normalize. The pressure from Russian oil firms to chase market share and lift investment restrictions flies in the face of what remains an oddly uneven demand recovery. Price recovery, however, no longer offers as much economic relief because the ruble has decoupled so significantly from the oil price via the budget rule and targeted currency intervention. The ruble doesn’t strengthen much to reduce inflation for imported goods and higher oil prices tend to reinforce higher domestic inflation levels overall. Even if one takes the best case scenario for oil, it actually poses downside risks for the Russian economy save some capital inflows into Russian securities unless the state spends money building stuff and sustaining capacity expansions for businesses.

The Central Bank has revised its profit forecasts for the banking sector upwards from 1.5-1.7 trillion rubles ($20.49-23.22 billion) to 2 trillion rubles ($27.32 billion) for 2021. So long as there aren’t any other shocks, the lending expansion that sustained the economy last year and in 1Q will roll ahead, slowed by expected rate hikes though they’d also increase interest earnings. There are some leading indicators that should give us pause. The growth rate of unsecured borrowing by retailers accelerated in May vs. April — 1.6% vs. 2.2%. Overall, it’s clear that Russian corporates aren’t facing any debt problems. The pain is going to really be felt by households. But the unsecured borrowing by retailers reflects both the burst of demand working itself out and also uneven impacts of price control measures and inflation on companies’ profits:

Retail borrowing — Red = annualized growth, LHS Blue = monthly growth rate, RHS

Retailers are really starting to borrow more, which indicates to me that wholesale prices are rising while profit margins aren’t yet keeping pace. There’s also the issue of the components of banking sector profits and their distribution, neither of which is well spelled out by the CBR’s report (consciously I think).

MinEnergo is looking for a way to structure the repayment of debts owed by Rosset’ subsidiaries in the North Caucasus to utility operators running power plants. They’ve asked the energy firms not to seek to recoup their debts via the courts till November to give the ministry time to sort it out. It’s an evergreen problem for firms in the region that are saddled with the task of eating losses to sustain the viability of federal transfers for regional budgets and the devil’s bargains constantly struck by Moscow tryin to manage local elites while staffing formal political posts with friendly faces and giving the security services leeway to act as needed. COVID and the newer surge in prices are stretching these arrangements further. In Dagestan, for instance, energy debts from consumers had risen 17% year-on-year as of early June for a total of 6.9 billion rubles ($94.32 million) where the average wage (not even median!) wage is around 29-30,000 rubles a month (about $400). MinEnergo is forced to use moral suasion and political pressure now. Energy firms rejected a previous proposal from Rosset’ to divvy up repayments from end users based on their tariff rates — basically Rosset’ wanted consumers buying power at auction on wholesale markets to pay in relation to their share of spending on electricity, guaranteed suppliers, and the upkeep spent to maintain power networks. Up to 100% of the debts owed are to be restructured in these proposals. Firms have little reason to trust that consumers in the North Caucasus are going to be in such great shape as to cover things so I’d expect MinEnergo will have to finesse some sort of additional guarantees or money out of Moscow. What are normally nuisances for the regime can become much bigger problems in a climate of high inflation and no fiscal policy intervention.

COVID Status Report

16,715 new cases and 553 deaths were recorded for the last day. That’s a drop in net cases, but the death toll is higher and also a lagging indicator compared to infections. To emphasize just how much the Kremlin has shifted following public opinion and regional governments, they’re now selling the line that people without immunity are a risk to others and some discrimination against them may be necessary. Regional hospital systems and medical services are being stretched again by the surge. Topping it all off, the end to flight restrictions with Turkey now has Russians scrambling to swap Russian holidays for time at Turkish resort and beach towns. It’s pushed the price of Turkish vacations up 20%. As more regions look to mandate vaccinations for key professions, the governor of Leningrad oblast’ Aleksandr Drozdenko has launched voluntary COVID passports for businesses to show regional authorities how many of their staff have been vaccinated. Vaccinate enough people, your business is exempt from restrictions. The state is now building competitive incentives for businesses to force their employees to get their jabs. Novogorod oblast’ is experimenting with a longer timeline, mandating that as of October 1 everyone going to work has to prove their vaccinated or get tested for COVID once a week. The case fatality rate appears to have peaked, which is a decent sign that the early measures are helping in some way. We need another week or two to see if vaccination uptake meaningfully picks up as people face actual substantive consequences for failing to get their doses.

Like what you read? Pass it around to your friends! If anyone you know is a student or professor and is interested, hit me up at @ntrickett16 on Twitter or email me at nbtrickett@gmail.com and I’ll forward a link for an academic discount (edu accounts only!).